- The semiconductor supply chain has been suffering capacity constraints since H2 2020, with both TSMC and Intel guiding more than 18 months of supply tightness ahead.

- We believe the shortage will be prominent at relatively mature nodes across 200mm and 300mm foundries due to strong demand from multiple sectors.

- Further, we expect the lingering demand-supply imbalance to continue, with prices seeing another round of hikes of at least 10-20% in 2022.

- To tackle the shortage, TSMC has revised up its 2021 capex guidance to $30 billion while Intel will work more closely with clients to seek solutions.

The global semiconductor supply chain has been suffering severe capacity constraints since H2 2020 due to pent-up demand in different sectors. Foundry capacity remains largely booked with fully-loaded utilization rates across different process nodes. Our checks suggest some IC design companies have already experienced 30-40% price hikes in certain product categories in 200mm foundries when compared with H2 2020. Therefore, we are looking at a new normal here.

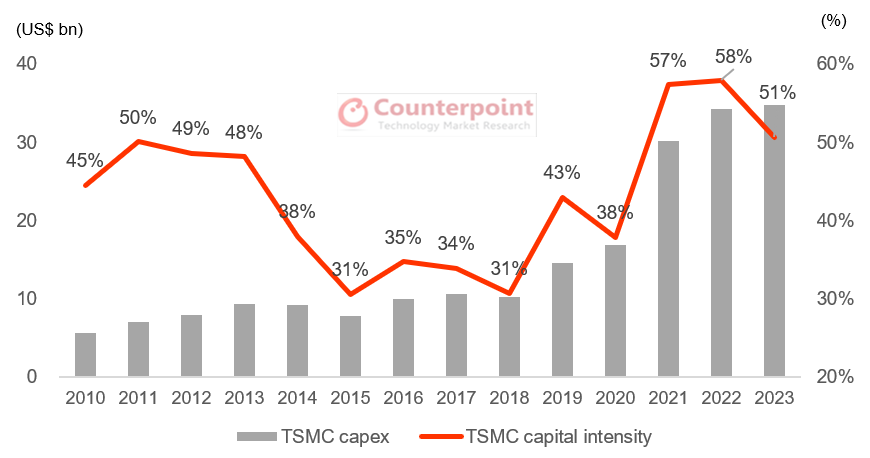

TSMC’s $100-bn plan for capacity expansion

TSMC, the largest foundry vendor in the world with ~55% market share, has revised up its 2021 capex guidance to $30 billion (from the previous guidance of $25-28 billion in January 2021), with 80% of this being meant for advanced node investments (3/5/7 nm), 10% for advanced packaging services and 10% for specialty technologies.

During the Q1 2021 earnings call, TSMC also reaffirmed its $100-billion capex plan for 2021-2023, mainly supported by customers’ promising outlook and commitments, which could translate into 10-15% CAGR of the USD revenue during 2020-2025.

Exhibit 1: TSMC’s Capex and Capital Intensity

However, TSMC and Intel have both highlighted that the overall semiconductor demand-supply mismatch will continue until the end of 2022, with capacity expansion failing to keep up with the skyrocketing demand, especially at certain mature process nodes. In general, the semiconductor industry is going through a significant structural demand shift. Therefore, both foundries and customers are on the same page in maintaining a higher inventory level to deal with uncertainties.

Decelerating capacity expansion and demand rally push up foundry costs

Recently, some foundry companies announced capacity expansion plans. These include TSMC’s 28 nm plant in Nanjing, UMC’s 28 nm in Southern Taiwan and Vanguard’s acquisition of another 200mm fab in Hsinchu. Supported by a few vendors’ de-bottlenecking expansion, we expect major additional capacity to be created at comparatively mature nodes soon.

Migration from 200mm to 300mm in the past few years has been too slow to eliminate supply constraint risks on mature nodes. Now, foundries are getting less support from the 200mm equipment vendors. Therefore, with the capacity failing to fulfill incremental orders and demand popping up in the short term, price hikes will emerge. We have even witnessed 30-40% price hikes on specific process nodes, apart from a generally 10%+ extra cost to design houses.

Unfortunately, this rise in prices will not stop in 2021. In order to secure 2022 capacity, design houses are negotiating with foundries. We foresee at least 10-20% higher costs here.

Intel foresees best days on solid demand

Intel has also shared a robust outlook, seeing its best days around the corner. Betting big on the tremendous demand for computing, the strength of its IDM 2.0 strategy, and ongoing technology investments, Intel expects to restore its leading position in the semiconductor industry. The company has also announced a capex plan of ~$20 billion for 2021, up 35-40% YoY and covering expenditure on two fabs in Arizona ($20 billion in total).

5G phone, HPC and automotive drive foundry capacity expansion

In terms of sales growth drivers, we believe smartphones will continue to play an important role for at least three years due to the 5G smartphone replacement cycle. Nevertheless, smartphone shipments growth has decelerated in recent years and is no longer sufficient to justify an aggressive capex plan and a robust sales growth outlook from foundry vendors.

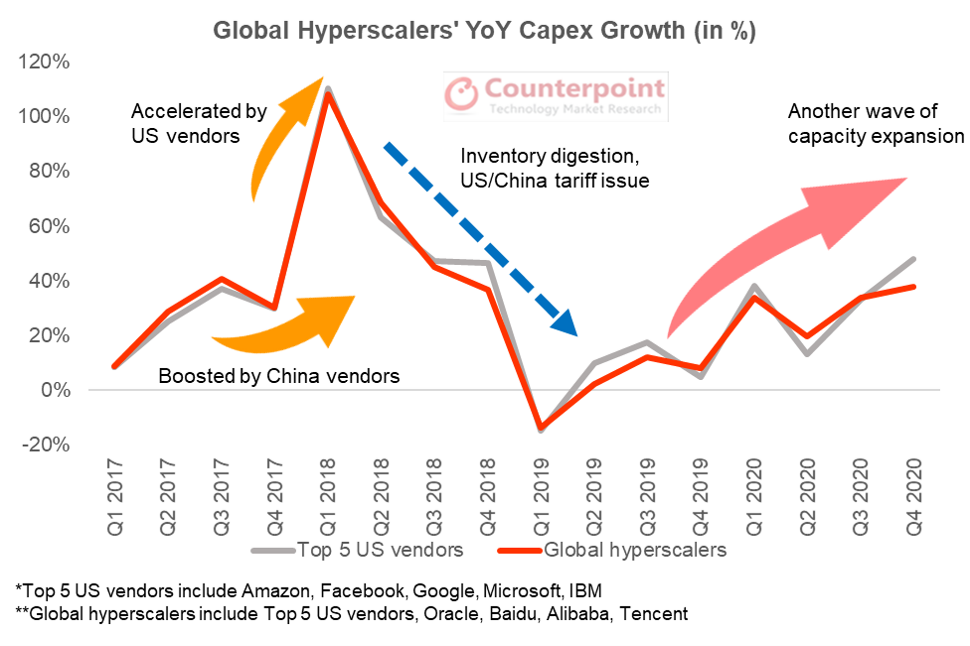

We believe high-performance computing (HPC) will step forward and consume a lot of new capacity for several years, mostly driven by emerging AI applications, connected devices, virtual reality/augmented reality and intelligent manufacturing. These segments require unprecedented computing power in both communication infrastructures and cloud data centers. Intel says nearly every application is now infused with artificial intelligence and machine learning. Global hyperscale data center vendors and cloud solution providers have put a lot of resources into capacity expansion. We believe this trend will continue to enhance computing power to support the sharp growth in HPC demand.

Exhibit 2: Hyperscale Vendors’ Capex Supports Worldwide Computing Power

Among the other sectors, automotive-related categories (electric vehicles, autonomous driving, charging devices) are expected to gradually become semiconductor-consuming giants on increasing semi content per car and the V2X (vehicles to everything) ecosystem. TSMC has already marked the automotive market to be its top priority in the upcoming years though it only accounted for 4% of its total revenue in Q1 2021 (against 45% from smartphones and 35% from HPC).

Conclusion:

Foundry cost hike in 2021 has largely settled down while another price increase for 2022 is already around the corner. Design houses are in the process of negotiating foundry costs and capacity quota with chipmakers. We expect the demand-supply imbalance to last for another year, along with another round of price hikes of at least 10-20% in 2022.