The semiconductor industry’s foundry sector delivered above-expectation revenue growth in 2020. With tightening supplies from most global vendors, we expect 2021 to continue this momentum.

In addition to a favorable macro environment, such as COVID-19 leading to logistical challenges and trade tensions prompting increase in wafer bookings, the technology migrations in leading-edge nodes (7-nanometer and 5-nanometer) appear to be accelerating to meet the demand from 5G smartphones, game consoles and AI/GPU in cloud servers. On the other hand, new capacity additions across the industry remain rational, with the second-tier foundry vendors preferring to raise wafer prices against building greenfield fabs.

Here we highlight our four predictions for the global foundry industry in 2021, based on our bottom-up analysis and surveys:

Double-digit YoY sales growth again in 2021

In 2020, the foundry industry revenue reached about $82 billion, representing a 23% YoY growth. Despite this high base of 2020, the double-digit growth will persist in 2021. We forecast a 12% YoY growth with a total revenue of $92 billion.

We expect TSMC, Taiwan’s leading foundry service company, to keep outperforming the industry by posting 13%-16% YoY sales growth in 2021. TSMC is scheduled to hold its quarterly result conference in mid-January.

To be consistent with Samsung’s public information, our foundry forecast includes Samsung Foundry’s internal business (to LSI). We expect Samsung Foundry, driven by more order wins from external customers such as Qualcomm and Nvidia, to post a 20% YoY revenue increase in 2021.

For the overall industry, the double-digit growth in 2021 consists of both wafer shipment increase and like-to-like wafer price (ASP) increases, something which we rarely saw in previous cycles. In particular, 8-inch foundries, which have been reporting supply shortages from H2 2020, are acting as a catalyst in convincing some suppliers to raise their average wafer price by 10% in 2021.

Significant ramp-ups in 7/5nm by largely adopting more EUV layers

Both TSMC and Samsung will beat the average industry growth rate due to their accelerating production ramp-ups of EUV-enabled nodes (7-nanometer and 5-nanometer, or 7/5nm) after passing through the initial stage of learning in 2019 and 2020. The EUV (extreme ultraviolet lithography) adoption is a critical factor in extending the Moore’s Law to consistently increase the transistor density of chips to enable the development of both 5G smartphones and HPC (high performance computing) applications.

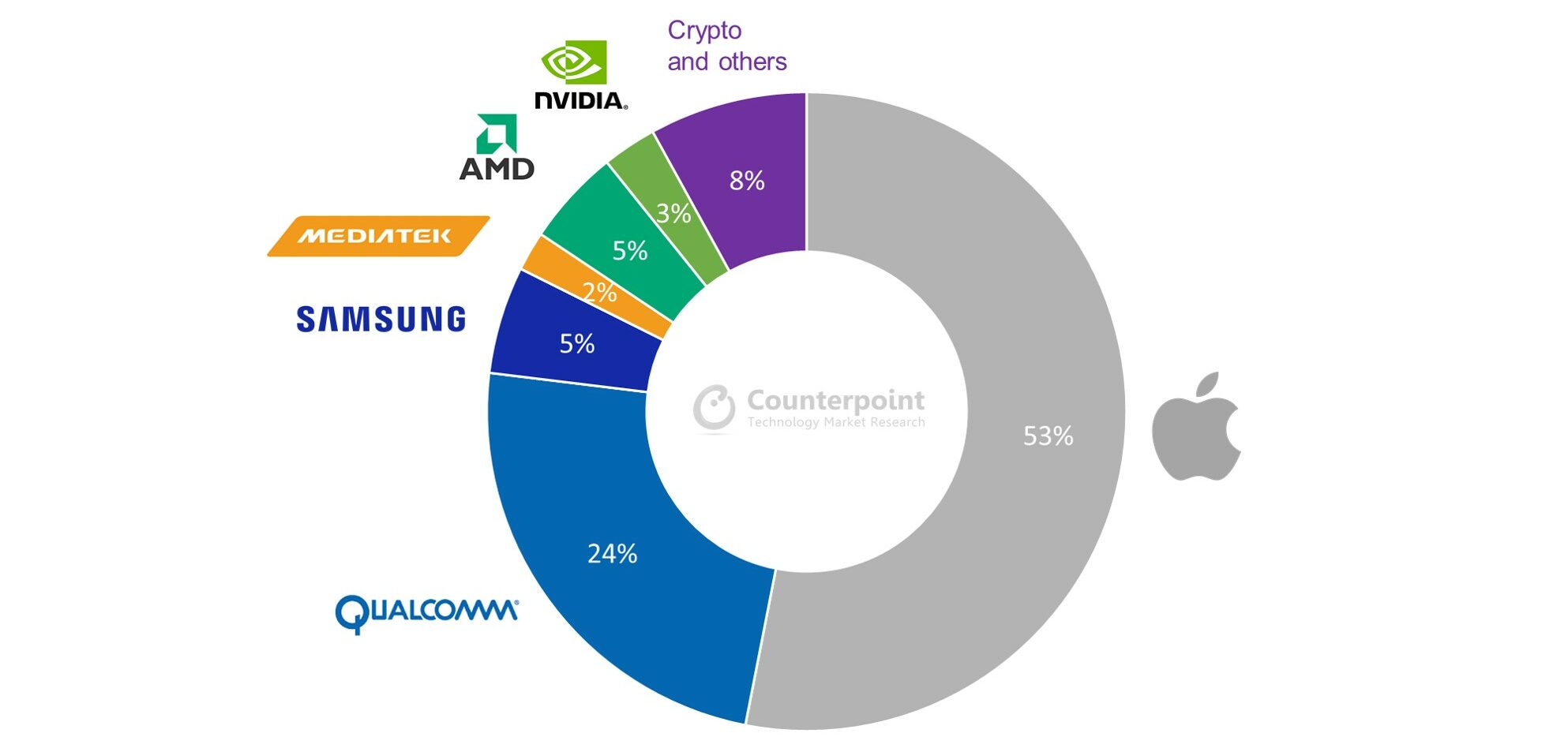

- 5nm: TSMC started its 5nm mass production from Q1 2020, and Samsung followed after 6-9 months. 5nm is considered a fully adopted EUV node for both foundries as Intel’s equivalent 7nm announced another delay in production last year. Based on our estimates, the total wafer shipment volume of 5nm will account for 5% of 12-inch wafers in the global foundry industry in 2021, up from less than 1% in 2020. Apple is the top customer (with all orders to TSMC) in 5nm this year (see Exhibit 1), including both for iPhones (A14/A15) and the newly released Apple Silicon. Qualcomm will be the second-largest 5nm customer as the iPhone 13 may adopt its X60 modem. TSMC is expected to book $10-billion revenue from 5nm in 2021. Samsung Foundry will also gain good traction from 5nm order wins, including its in-house (Exynos) SoC and Qualcomm. In our view, the capacity utilization rate will reach an average of 90% for TSMC and Samsung in 2021, with the upside from stronger flagship 5G smartphone models.

Exhibit 1: 5-nanomater Wafer Shipment Breakdown by Customer, 2021

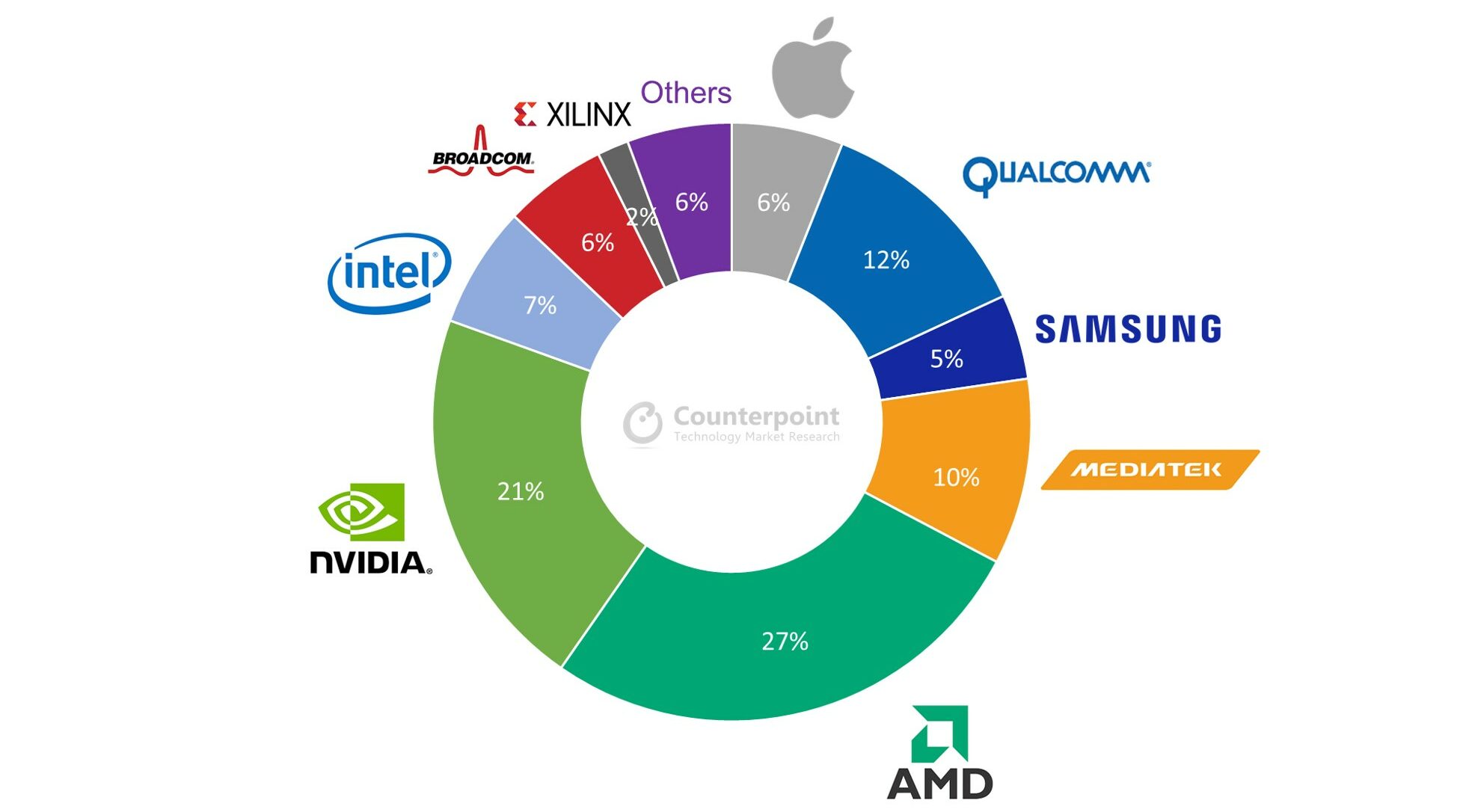

- 7nm: Different from 5nm, with over 80% wafers used in smartphones, the 7nm applications are more diversified into AI/GPUs, CPUs, networking and automotive processors. TSMC has a variety of 7nm (DUV only), 7nm plus (with EUV) and 6nm (with EUV) in its 7-nm family, while Samsung has introduced 7nm/6nm with both adopting EUV production. Based on our estimates, the total wafer shipment volume of 7nm will account for 11% of 12-inch wafers in the global foundry industry in 2021. In this geometry, smartphones will only consume 35% of wafers (see Exhibit 2) and the majority will ship to AMD (27% of 7nm shipment volume) and Nvidia (21%). In the light of stronger demand for game consoles, cloud server/AI processors and mainstream 5G smartphones, the capacity for 7nm looks extremely tight through the whole of 2021, with the average utilization rate at 95-100% based on our calculations. Therefore, for emerging demand such as crypto-mining ASIC and ARM-based processors (in server and auto), the chipset vendors and OEMs will find it difficult to get allocation for extra capacities in the near term.

Exhibit 2: 7-nanometer (N7, N7+, N6) Wafer Shipment Breakdown by Customer, 2021

A high level of chip inventory becomes normal through the year

Although the foundry industry is less cyclical than that for IC memory, we still consider inventory level as one of the major factors to predict growth. However, we need to reset the expectations for 2021 or even for early 2022 as long as COVID-19 and global trade tensions persist. Global OEMs, as well as their IC vendors, are willing to prepare for extra levels of components. The procurement lead time of some standard ICs in the channel, according to the component supply chain, has lengthened to 26 weeks (6 months) and above from late 2020. In other words, we might see an ascending wave of double-booking pattern in matured nodes not only on TSMC but also more seriously on the second-tier foundry vendors.

By the end of Q3 2020, based on the financial reports from major global IC fabless companies, the inventory was about 79 days compared to the industry average of 70 days since 2016. If we see recent comments from AMD, Nvidia, Qualcomm, or even smaller players like Dialog Semi (analog ICs), the prospects of 2021 are generally upbeat on 5G smartphones, WFH devices and cloud server spending. The momentum supports high inventory levels. As long as the concern of supply chain disruptions persists, chip vendors would maintain a high level of inventory from Q4 2020. The argument indicates a better-than-normal seasonality in H1 2021, since foundry customers would choose to place wafer orders earlier to avoid capacity risks in the second half. We expect the industry inventory to hit the peak during the middle of this year.

Capital intensity also maintains high level, given upside from wining IDM shares

While we will wait for ASML’s EUV shipment forecast and TSMC’s capital expenditure (Capex) guidance for 2021 (both expected in mid-January) as the key bellwethers of global semi outlook, the market expectation of TSMC’s record-high (over $20 billion) number in 2021 looks reasonable to us. In our view, it will be a crossover year for TSMC’s sales between its two growth pillars – smartphone and HPC.

We see Intel going in for CPU outsourcing soon for its long-term survival. Both TSMC and Samsung are ready for the opportunity by potentially starting to expand their 5nm/3nm capacities during the year. It looks like the capex-to-sales ratio, as an indicator of future revenue growth confidence for chipmakers, will maintain peak levels in 2021 – 40% for TSMC and 70% for Samsung Foundry. Aside from the strong demand of end applications, which we discussed above, IDM outsourcing trends are accelerating for global IC vendors pursuing profitability. Not only from Intel, TSMC is likely to see growing orders from Japanese customers including Sony’s CIS (48MP) and Renesas’ MPU (at 28nm) during late 2021.

Conclusion

The upcycle in foundry industry during 2020-21 contains both multiple cyclical and structural positive drivers, which we have not seen since the tech bubble years (1998 -2000). The incremental demand of foundry industry will come from most sub-sectors, including automotive, to support its double-digit growth in 2021. Moreover, by factoring in IDM outsourcing, we expect the industry to reach and exceed $100 billion of market size during 2022-23.