To receive weekly updates on the COVID-19 situation and our latest research straight to your inbox, click this link to register

Click here to get the latest weekly updates on the COVID-19 situation and its impact and implication on the various sectors.

Week 22: August Auto Sales Update – Key Markets Indicate Recovery

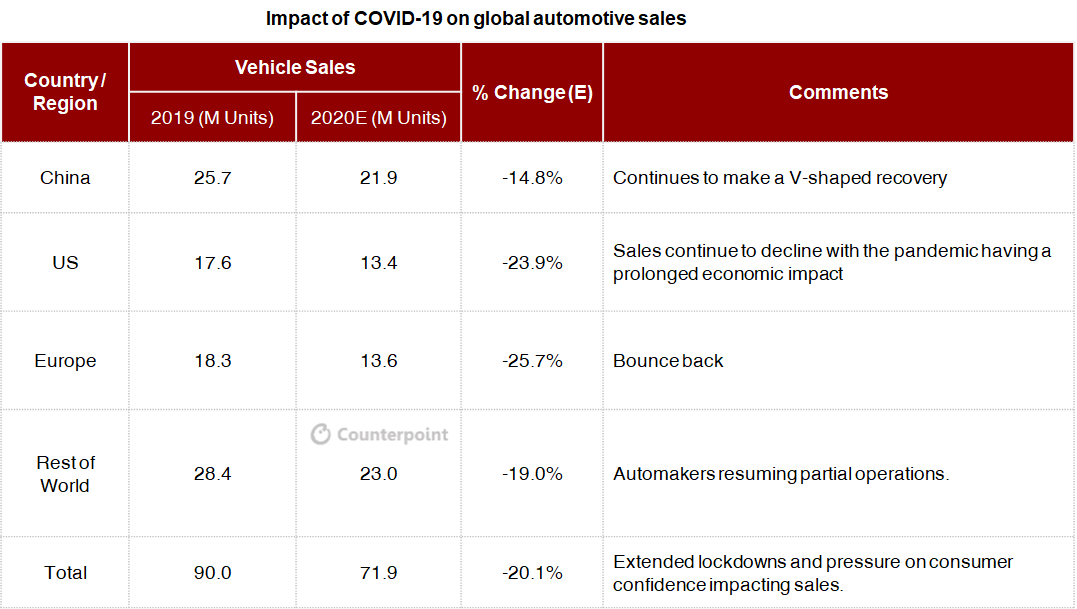

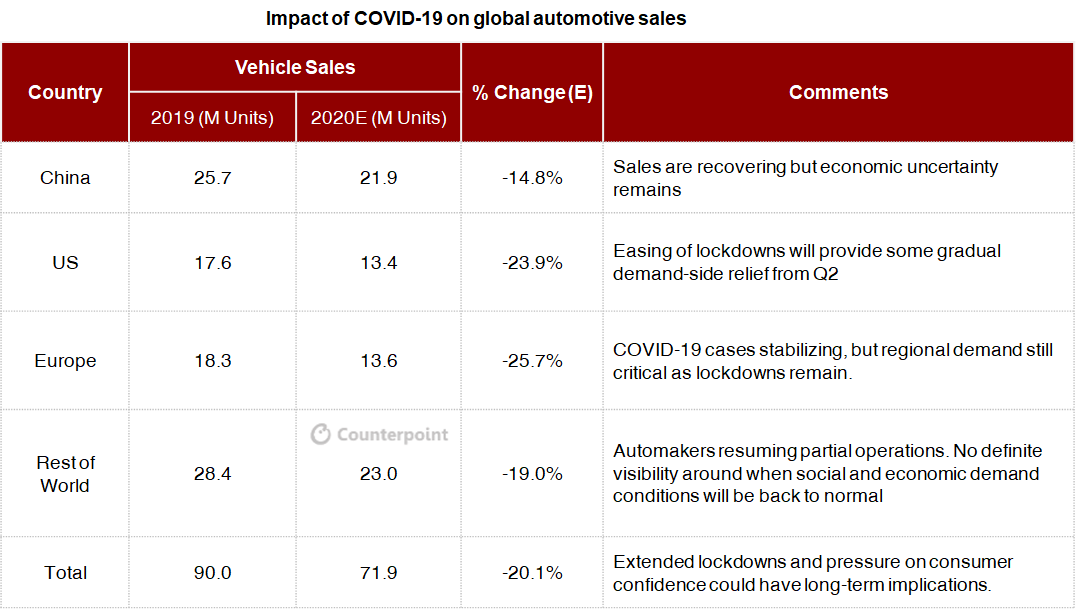

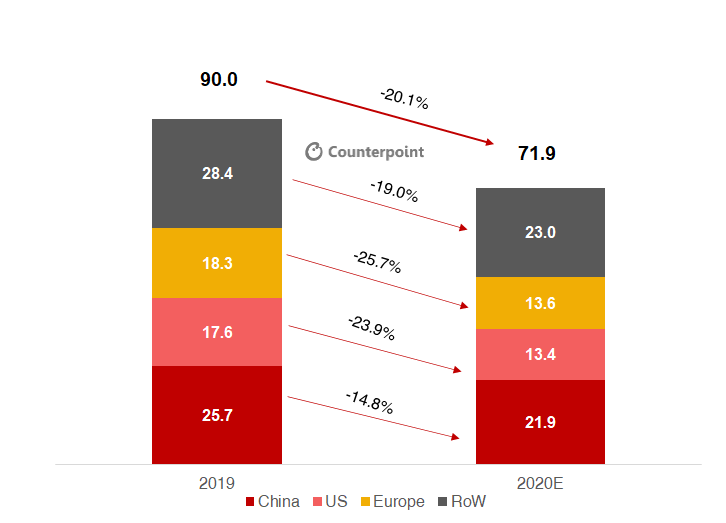

While many key markets saw signs of improvement in August on month-on-month (MoM) basis, it remains difficult to ascertain the actual market situation as the pent-up demand may be covering up a lower intrinsic level of market demand. Moreover, there is always a risk of a second wave of COVID-19. As a result, Counterpoint analysts continue to hold on to their 2020 annual outlook of nearly 20% decline over last year, with global passenger vehicle (PV) sales estimated at around 71 million units.

United States

Automotive industry in the US continues to remain fragile. Vehicle sales in August declined close to 20% (YoY), reaching 1.33 million units, despite an extended weekend due to Labor Day falling on a Monday. Total January-August 2020 sales reached around 8.8 million units, down 23%. During the month, Toyota saw a sharp decline of 24.6%, followed by Honda (-23%). Hyundai, on the other hand, performed comparatively better with only an 8.4% decline. Limited inventories and fewer incentives continued to hold back sales.

China

China automotive sales continue their fast recovery. Vehicle shipments reached close to 2.2 million units in August, up 11.6% on YoY basis. Total shipments during January-August 2020 were down 10% on YoY basis. Counterpoint expects the recovery to continue in coming months driven by improving car-buyer sentiment (especially in affluent classes) and pro-NEV (New Energy Vehicle) policies like scrapping of vehicle purchase tax on NEVs and extension of subsides till 2022 with a slower phase-out pace. In June, the government announced to increase the NEV credit ratio by 2 percentage points every year till 2023, from 12% in 2020 to 14% in 2021, 16% in 2022 and 18% in 2023.

Europe

Easing of lockdowns in many countries coupled with stimulus packages to support economic revival seems to have started benefitting the region’s automotive industry. Vehicle sales in August crossed 1.2 million, declining 16% on YoY basis. Despite the decline, this was a good performance considering sales in August 2019 were high as automakers rushed to push their uncertified vehicles before the September 1, 2019 deadline for the Worldwide Harmonised Light Vehicles Test Procedure (WLTP) testing.

Other Markets

Japan: Vehicle sales in August crossed 326,000 units, declining 16% on YoY basis. Counterpoint remains cautiously optimistic for coming months as resignation of Prime Minister Shinzo Abe could adversely impact the market.

South Korea: New vehicle sales in the country from top five automakers — Hyundai, Kia, Ssangyong, Renault and GM — declined close to 6%, reaching around 112,000 units. In June, the government extended the 30% cut in consumption tax on passenger cars till December 2020, benefiting sales.

Other Asia: While the year-to-date sales have seen a considerable decline, they are improving on MoM basis. Key markets like India are seeing recovery in MoM sales due to easing of lockdowns.

Author: Aman Madhok

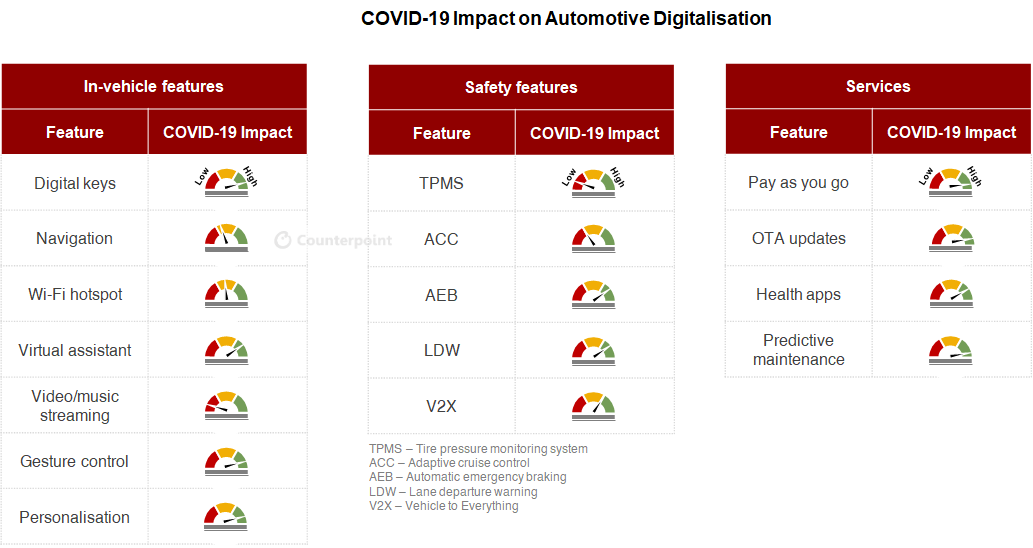

Week 21: Connected Car Gets Pandemic Push

The COVID-19 pandemic has led to many changes in car-buyer behaviour and attitude. Digital services and features are being readily accepted by people as a way to stay connected, trackable and safe. Increasing penetration of in-vehicle screens will lead to easy integration of many of these digital features. This blog identifies and compares key digital features and services available for cars, and which among these will benefit due to changing lifestyle and behaviour of people.

In-vehicle features

In-vehicle digitalisation is expected to increase as people spend more time in their personal vehicles (compared to public transport). Popular connected features include navigation, digital keys, and Wi-Fi hotspot. Among these, digital keys will see a high demand in the coming years due to its low-cost implementation. Virtual assistant, voice recognition, personalisation and gesture control will also see increasing demand on growing concerns over touching surfaces.

Safety features

Safety features to prevent accidents, such as automatic emergency braking (AEB), lane departure warning (LDW), head-up displays and surround cameras, are expected to gain popularity. Convenience features like automatic cruise control (ACC) are expected to see a limited impact from the pandemic. Nevertheless, since many times these safety features are sold as bundled packages, COVID-19 will aid in their penetration.

Connected Living

Cars are expected to have seamless integration with home, infrastructure, and other devices promoting vehicle to everything (V2X) technology. Increasing coverage of 5G networks will allow seamless integration of cars with other devices and ecosystem. Vehicle to pedestrian (V2P) communication, in particular, will see development. However, high investment involved in developing a V2X technology could delay its implementation.

Services

Connected services promoting social distancing and reduction in the number of garage trips will see a rise in coming years. Pay-as-you-go services will enable touchless transactions for refuelling, toll payments and purchasing on the go, among others. OTA updates will become popular, restricting unnecessary trips to service centres.

Health and location related apps are expected to gain popularity, aiding family members to track the location and well-being of their loved ones. Recently, GM launched a smartphone-based app, Guardian, which uses phone sensors to detect a crash and inform emergency services. Other features of the app include location status and roadside assistance.

Conclusion

Digitalisation in cars will get a boost from COVID-19 with people embracing a digital life that promotes social distancing, safety, tracking and efficiency. Services and features enabling the above will see growing popularity among car-buyers. Digitalisation will also be supported by other factors like increasing screens in cars and increasing 5G network coverage.

Author: Aman Madhok

Week 20: Global Vehicle Sales Remain Fragile

Global passenger vehicle (PV) sales declined by nearly 7% YoY in July, despite regions showing varied signs of month-on-month recovery from COVID-19 induced lockdowns. Overall, cumulative YTD global PV sales are down by 25% YoY through July.

While most regions are certainly seeing signs of improvement, it remains difficult to ascertain the actual market situation. Pent-up demand remains the most important contributor to recovery, which may be covering up a lower intrinsic level of market demand. As a result, Counterpoint Analysts continue to hold onto their 2020 annual outlook of nearly 20% decline over last year, with global PV sales estimated at around 71 million units.

China

The Chinese PV market continues to make a V-shaped recovery, with July volumes climbing 16% from a year earlier, a fourth consecutive month of improvement, stepping up sales to a higher gear from nearly 7% YoY growth in June. While July PV sales in China rose to 2.1 million vehicles, on a YTD basis cumulative volume have dropped 13% from last year’s 12.4 million vehicles.

Sales of new energy vehicles (NEVs, i.e. battery-powered electric, petrol and electric hybrid and hydrogen fuel-cell vehicles) in July ended 12 consecutive months of YoY declines, with a 20% uptick to nearly 98,000 units. This sale spike possibly demonstrates that NEV OEMs and customers are now at terms with the lowered government subsidies since last year. Counterpoint estimates NEV sales at over 1.1 million vehicles in 2020, a decline of 11% from last year. Continuing to lead the pack of fully electric vehicles, Tesla sold 11,000 vehicles in July while BYD took the lead position in total NEV sales, delivering over 14,000 units.

With China’s economy still recovering, and the possibility of a second wave of the virus still looming, Counterpoint is holding to its earlier base case forecast of nearly 22 million PV units for 2020, an almost 15% decline from previous year.

United States

Sales in the US continue to drift with the pandemic having a prolonged impact on the country’s economy. July PV sales volume, though up versus June, is down nearly 19% YTD compared to the previous year. Fleet sales too continue to remain weak, with July volumes falling by nearly 30% of the volumes reported in June.

COVID-19 continues to spike in key US states, including California, Texas and Florida, resulting in curbs on movement of citizens and strong headwinds for the country’s PV sales. All this while the industry continues to reel from the effects of earlier lockdowns and “shelter in place” directives that had closed thousands of dealerships in March, April and May.

Counterpoint analysts are holding to their earlier forecast for the US — a 24% annual decline for 2020, estimated at around 13.4 million units.

Europe and United Kingdom

PV registrations in Europe dropped 5.7% in July, with government incentives and lifting of lockdown restrictions having stimulated sales demand back to near pre-pandemic levels. However, from a year-to-date perspective, Europe is tracking an overall decline of 36% for the same period last year. Counterpoint analysts estimate Europe sales to fall by almost 26% this year to 13.6 million vehicles, with key factors like lowered government subsidies and possible resurgence of COVID-19 lingering.

In the UK, PV sales rebounded in July as dealers reopened with easing of coronavirus lockdowns, even as battery electric vehicle sales continued to surge. Based on sales data released by the Society of Motor Manufacturers and Traders (SMMT), British new car registrations rose by almost 11% YoY in July to nearly 175,000 units. July is the first full month of business in the UK after car dealerships were allowed to reopen.

Notwithstanding the signs of a slight bounce-back, Counterpoint analysts remain cautious. European and UK consumers are still wary about buying high-ticket items like cars, given the uncertainty over the economy.

Rest of World

India’s domestic auto industry may have turned the corner in July, with monthly declining trends flattening out. For the first time in several months, the Indian auto industry reported a single-digit decline of 1% in passenger car wholesales, with 198,000 units being shipped last month compared to 200,500 units in the same period last year. July shipments are likely the low point of a V-shaped recovery as Indian states increasingly ease lockdown measures and more dealerships open in key urban centres. The industry still needs to demonstrate a sustainable demand trend, at least over the medium term. As OEMs in India continue to resolve challenges with the supply chain, they will also need to procure buffer stocks of material to protect themselves against future lockdown disruptions.

Japan’s PV sales continue to improve, with a relatively moderate 14% YoY decline in July, compared to a 45% YoY decline in May. Consumers are preferring purchase of smaller-sized vehicles to avoid crowded public transportation. Sales of Mini Vehicles (engine size smaller or equal to 660 cc) currently account for nearly 40% of total car sales. However, with the recent sharp rise in new COVID-19 cases, and possible enforcement of movement restrictions, the recovery in sales is expected to slow down.

In South Korea, the selling rate has slowed down from an all-time high in June, with the first phase of a temporary excise tax cut on passenger vehicles expiring at the end of the month. The market, however, continues to perform reasonably well, with sales having increased YTD by nearly 8%. Sales in H2 2020 are expected to be sustained with an anticipated announcement of the second phase of the temporary excise cut, which has proven to have been a key factor in stimulating demand recovery in Q2 and Q3.

Revised Global Automotive Outlook

While varied signs of a fragile recovery continued to emerge in July, Counterpoint Research remains cautious and is holding to its earlier global automotive sales outlook of around 72 million units for 2020, an over 20% decline from 2019.

Author: Vinay Piparsania

Week 19: Used Car Sales Start Recovery in Key Markets

Used cars are seeing recovery in key markets not only owing to hygiene concerns amid the COVID-19 pandemic but also reduced car-buyer budgets due to economic downturn. Dealers have started to report increasing (or holding) residual value of used cars, indicating the increasing demand. Increased focus on online sales by automakers, dealers and third-party e-commerce companies is also benefiting the sales of used cars. This blog lists recent positive developments in key used vehicle markets, indicating a much faster recovery for global used car sales when compared to new cars.

US

- Leading online used car platform Carvana reported 43% increase in sales during Q1 2020. The company has plans to expand to 100 new markets in the US.

- Carmax, the leading used car dealer in the country, called back 155,000 furloughed employees (around two-thirds of its workforce).

According to online platform Edmunds, the average listing price of used vehicles increased by $708 in July when compared to June, reaching $21,558.

India

Used car market size in India is around 1.4 times higher than that for new cars (compared to 4-5 times in the developed world) and has a huge growth potential. Used car sales had been growing at a much faster rate during pre-COVID-19 times and industry participants are already seeing recovery in such sales:

- Leading used car online platform Droom announced that the traffic on its platform was up by 175% and leads were up by 250% during the April-June period. During the same period, Maruti Suzuki True Value reported used car sales increasing 15% compared to last year.

- Mahindra First Choice Wheels also reported higher demand in June compared to last year.

Europe

While both new and used car sales continue to decline in many European countries, the rate of decline was steeper for new car sales during Q1 2020 in key markets like the UK, Spain, Germany and Italy.

China

The fall in used car sales has slowed down in China after the market contracted by 67% (YoY) during Q1 2020. According to the China Automobile Dealers Association, used vehicle deliveries declined from 1.6% to 1.2 million in June, but the deliveries were up 4% compared to May.

Early Signs

Given the fluid conditions, the early signs of growing used car sales need periodic tracking and should not be generalised as a global trend due to the following reasons:

- Lower inventory of new cars could momentarily drive used car demand. With auto plants reaching 100% production levels, used car sales could see a decline in coming months.

- If driven by pent-up demand, the sales could see a decline in coming months.

- Customers can hold on to their old vehicles for a longer time, creating an inventory shortage for used cars.

- Used car market growth will vary from country to country depending on government policies, economic recovery and customer sentiments.

Conclusion

Despite the uncertain conditions, it is expected that the used car market will see a much faster recovery from the pandemic when compared to the new car market, considering the strong drivers like growing need for personal vehicles and budget constraints.

Author: Aman Madhok

Week 18: India’s July Automotive Sales on Choppy Recovery Track

India’s domestic auto industry may have turned the corner, with monthly declining trends flattening out, suggest July sales reports.

For the first time in these last few months, the Indian auto industry has reported a single digit decline of just over 1% in passenger car wholesales, with 198,000 units being shipped last month compared to 200,500 units in the same period last year. July shipments are likely the low point of a V-shaped recovery as Indian states increasingly ease lockdown measures and more dealerships open in key urban centres. The month has shown significant wholesales improvement in both two-wheelers and passenger vehicles, indicating significant pent-up demand across the country.

Counterpoint expects to see further improvement in monthly vehicle sales, with new product launches planned, supply chain stability and incremental demand from rural India as the country moves into its traditionally high-selling festive season. We expect extraordinary promotional offers by dealers and automakers to continue, encouraging consumers to visit showrooms and consider purchasing new vehicles.

Choppy recovery across the country

The July automotive sales distribution pattern, however, shows that recovery from the pandemic not only varies in speed across the country, but is also uneven. This can be attributed to the length of lockdowns in different regions, the underlying economy of a region, consumer confidence, availability of finance and incentives offered by dealers. Broadly, retail sales are recovering faster in semi-urban and rural areas, which have been relatively less impacted by the spread of COVID-19.

Many regions continue to remain vulnerable due to their limited ability to manage further outbreaks of the virus. Intermittent and sudden lockdowns being re-introduced in some states, such as Uttar Pradesh, Maharashtra and Bihar, are negatively impacting the fragile consumer confidence and spending.

While leading automakers Maruti Suzuki and Hyundai have seen a steady recovery in vehicle production and shipments since the unlocking in May, we believe sustaining the retail sales momentum will be a challenge as pent-up demand winds down. While some states could recover faster, the overall longer-term forecast is that some cities and states will take till the year end to recover annual sales volumes to pre-COVID levels, and some possibly not at all.

Let us look at the performance of some of the key players in the passenger car and two-wheeler categories over the month:

Passenger cars

Maruti Suzuki posted a 1% growth, with 100,000 units shipped last month against 101,300 in July 2019. While marginal, it does signal green shoots of recovery ahead with an almost 50% increase in mainstream hatchbacks — about 17,300 units shipped in July. This also demonstrates growing demand for safer, personal mobility options. In addition, Maruti Suzuki is planning to launch a range of compact SUVs in the second half of 2020, enhancing its offerings in this relatively resilient category.

Hyundai too is moving closer to full recovery, having shipped 38,200 units in July versus 39,000 units last year, a 2% YoY decline but a significant improvement against the 79% YoY decline recorded in June. Hyundai continues to have a strong order book for its refreshed Creta SUV, the newly launched Venue Crossover and, surprisingly, for its updated Verna sedan.

While Mahindra & Mahindra has reported a 35% YoY decline with shipments of 11,000 units last month, we expect sales to improve over the rest of the year. Revival in demand for its vehicles is expected to be sustained in rural and semi-urban areas. The scheduled launch of popular utility model Thar in a refreshed, contemporary and feature-loaded avatar, and in time for the festive season, will provide an additional push.

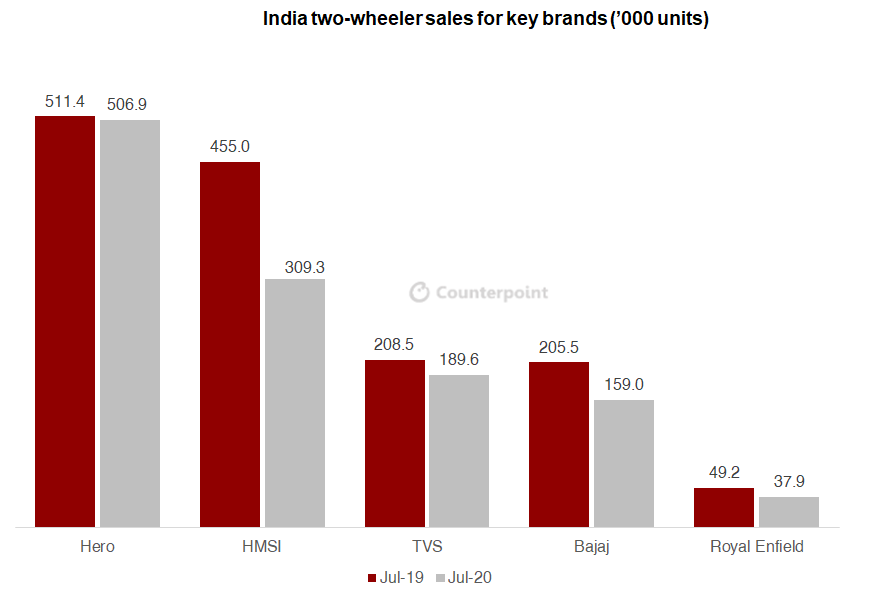

Two-wheelers

India’s, and also the world’s, largest two-wheeler manufacturer Hero MotoCorp has reported a marginal YoY drop of less than 1% in July. It is running at over 95% of its production capacity, signalling a healthy rebound. The company’s July shipments saw 14% sequential growth over June. While the numbers primarily show signs of recovery, they also confirm that supply chain issues, such as the availability of workers and raw material, have been resolved considerably.

Till the COVID-19 pandemic is brought under control, Counterpoint expects the country’s two-wheeler segment to continue to grow much faster than passenger vehicles, being a cost-effective personal mobility solution and also popular among Indian commuters.

Conclusion

Counterpoint believes that while July sales may signal the start of a recovery trajectory, the industry still needs to demonstrate a sustainable demand trend, at least over the medium term. As OEMs continue to resolve challenges with the supply chain and scramble to replenish inventories, they will also need to procure buffer stocks of material to protect themselves against possible future disruptions due to re-introduction or extension of lockdowns.

Counterpoint analysts continue to remain cautious and are holding to their earlier forecast of a 25% decline in all categories in 2020 compared to 2019.

Author: Vinay Piparsania

Week 17: Car Subscription Services Get COVID-19 Push

The shift towards car subscription services, which started during the last few years, is only going to accelerate during the COVID-19 pandemic. Rising awareness about health among car- buyers is making them consider personal vehicles over public transport, with subscription payment models making vehicle ownership more accessible. This blog analyses the key drivers for subscription-based models and the role of COVID-19 in pushing this shift.

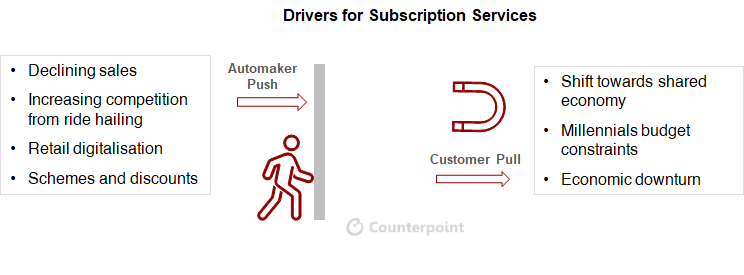

Why Subscription?

- Automakers are looking for new ways to push sales and make cars more accessible for customers in the wake of COVID-19 pandemic, which has put a lot of strain on their purchasing power.

- There is a generational shift towards a shared economy where everything from OTT to consumer electronics is being subscribed to. In mobility too, millennials are moving away from car ownership to shared mobility.

- Rental companies are offering flexible subscriptions ranging from 1 to 36 months and attractive schemes, like extended loan tenure, low down payment, no EMI for a year, return assurance and home delivery, to push sales.

- During COVID-19, dealers have shifted online to provide a quick, streamlined and hassle-free buying process, thus aiding in subscription sales.

Automakers Taking Subscription Seriously

While subscription services, including Volvo’s Care, Ford’s Canvas, Cadillac’s Book Porsche Passport and Mercedes-Benz’s Flexperience, were already available, more automakers are focusing on such services during COVID-19:

- India’s largest car manufacturer Maruti Suzuki has partnered with ORIX to start a pilot subscription model for new cars. Hyundai, the second largest player in the country, started its subscription service in 2019.

- In March, Nissan launched the ClickMobi car subscription services in Japan. The service is currently available in 23 of Japan’s 47 prefectures. The company plans to expand it to the whole country by September.

- In January, Toyota launched the Kinto subscription service across Europe. This includes Kinto One, a subscription-based service for new cars.

- In July, JLR launched the Pivotal vehicle subscription schemes in the UK, offering a six-month subscription starting at $934 a month for a Land Rover Discovery Sport or Range Rover Evoque. JLR expects subscription services to account for 10% of all car sales in the US and Europe by 2025.

- Volvo, which launched its subscription service Care in 2017, expects it to account for 50% of its revenues by 2025.

Mushrooming start-ups

Many start-ups, including ZoomCar and Revv, are collaborating with automakers and dealers to provide the software platform, schemes and expertise for subscription-based models. Third-party collaboration is helping automakers and dealers in a fast scale-up of their subscription offers.

- In July 2020, a London-based car subscription start-up secured €22.6 million in funding. The company provides subscription-based car buying in the UK in partnership with automakers including BMW, VW and Mercedes Benz.

- Australian start-up Loopit (earlier known as Blinker), which has around 500 dealerships on its software subscription platform, announced 52% increase in dealers wanting to integrate into the platform during the country’s initial lockdown period.

Conclusion

- In the short term, COVID-19 will accelerate the shift towards subscription models as car buyers refrain from lumpsum payments on big-ticket purchases. The need for privacy and social distancing will also push them towards such services.

- In the long term, shift towards a shared economy and growing competition from ride-hailing services will continue to encourage automakers to adopt subscription models to push car sales.

Author: Aman Madhok

Week 16: Need for more resilient supply chains

The COVID-19 pandemic has demonstrated how vulnerable automotive supply chains are to disruption, bringing under scrutiny the extended global supply strategies.

The abrupt closure of production centres in China and its domino impact, causing widespread chaos among global auto manufacturers, were felt progressively in Europe, the US, India and South America. Having offshored their manufacturing activities to low-cost countries, many automotive OEMs and suppliers are now scrambling to establish shorter or localised regional supply chains.

The drive to shorten supply chains

Even months before the COVID-19 outbreak, there was a growing interest among global automakers to localize manufacturing of critical components. Trade tensions were at their peak with the escalating tariff war between the US and China, resulting in a broader nationalistic spirit arising in some other countries too. The intensification of protectionism, through targeted financial trade barriers, had become a real and present threat for multinational auto operators to deal with.

With globalized supply chain networks currently programmed for the lowest possible price, most Western companies had set up centralised manufacturing facilities in lower-cost economies, where final products are assembled competitively and shipped to higher-income markets. Automakers, in particular, source parts and electronics from China, mainly because they are cheaper. However, rapid political developments, natural disasters and now the global pandemic have revealed the inherent weakness at the core of such a model of offshore manufacturing. For example, when the pro-Brexit (UK’s decision to leave the European Union) vote was announced in 2016, European auto OEMs and suppliers immediately planned for the worse and rushed to invest in new supply chain resources in the UK. While a change towards more flexibility and multi-level sourcing by the global auto industry had already begun cautiously, the COVID-19 impact has now made it a more definitive and urgent course of action.

Over the next few years, Counterpoint analysts expect to see a broad overhaul of the global automotive supply chain infrastructure based on the following trends:

Globalization to regionalization

Currently, most leading global automakers source 30% to 60% of their parts from China, including modules and sub-assemblies. Given the incredibly high number of parts required – each with different lead times – a return to regional supply chains does present an incredibly complex challenge. However, that challenge is being considered worth taking on by stakeholders for a post-COVID world.

Intending to establish alternative, flexible and adaptable supply chains — while mitigating single-source vulnerabilities – OEMs, component manufacturers and auto sub-system assemblers are now looking to strategically source, assemble and deliver from within their regional borders, and are also reconsidering setting up regional logistic hubs.

Fundamentally rethinking the supply chain

COVID-19 has exposed the weaknesses of a globalized manufacturing system, necessitating a fundamental rethink of existing supply chain operations. The distributed global business model, being primarily driven by an objective to achieve minimum cost, needs to be resilient. Supply chain models will need to be reconfigured, based on business optimization. Modifying the supply chain as a key business driver and bringing back timely human oversight are some critical factors that can bring inherent agility.

With volatility in production volumes and schedules expected to be a norm, suppliers and logistic operator chains will have to be adaptive, and be able to recover quickly from major natural and man-made catastrophic events such as earthquakes, floods, fires, industrial strikes and social unrest. Human overrides and protocols will need to be re-introduced to bring stability back to the global supply chain during such a crisis. As the current pandemic stress-test has demonstrated, large variances and disruptions cannot be managed through statistical and algorithmic models with such unusual events typically disregarded as “outliers” and overlooked in operational programming.

Resilience through re-shoring — easier said than done

Despite the pain caused by production losses, the business case for increasing supply chain resilience is not straightforward. Reconfiguring and reducing the length and complexity of global supply chains is not without its challenges. Inevitably, short-term costs will be a consideration, as well as the ability to recruit new staff with the requisite skills, knowledge and experience, and access to adequate capital.

With thousands of suppliers involved in a vehicle’s value chain, diversifying suppliers to increase resilience involves significant investments and recurring costs. Automotive components are typically sophisticated, intricately engineered, bulky and also fragile, with high logistics and transport costs. In most countries, government policies encourage sourcing from local producers by achieving a local content threshold to qualify for reduced import tariffs. However, even if such suppliers are considered as alternatives, they are required to be tooled, trained and resourced to produce to specifications and quality standards.

Nonetheless, the benefits of shortening supply chains are considerable, specifically greater security and increased resilience to causes of disruption. Although COVID-19 has brought these into focus, it is not the only risk to established OEMs. There is the ever-present threat caused by natural and man-made events, the ongoing trade disputes and tariff wars between major trading nations, and political instability in regions that supply critical raw materials, combined with a rise of nationalism and protectionism around the world.

The current configuration of international supply chains relies predominantly on low trade barriers and assurances that they will remain for a reasonable time period. Unfortunately, the devasting economic impact of COVID-19 has led to a resurgence of protectionist sentiments in most countries, and a highly probable threat of such benign policies being withdrawn. Further, the economic arguments for offshoring are not as persuasive as they used to be, with average wages in China’s manufacturing sector, for example, having increased over countries such Brazil or Mexico

There could be many other significant factors behind re-shoring decisions too, such as access to qualified personnel, skills, technology and innovation. Proximity to primary markets is another key consideration, as well as improved quality. OEMs look for quality at the most competitive cost. One of the advantages of working with local suppliers is their ability, if set up correctly, to deliver both. Working with localised suppliers also reduces challenges associated with communicating across multiple time zones, languages and cultures.

Among the deciding factors will be the types of components or aggregates being produced, along with market demand, speed of response and ability to supply custom-engineered solutions with short lead-times.

Conclusion

The sheer number of suppliers to the automotive industry, who are currently clustered in specific regions of the world, present major obstacles to diversifying risks. Reducing or expanding the number of suppliers is not necessarily the only way to configure resilient supply chains.

Counterpoint Research believes that ultimately we will see a combination of traditional extended supply chain models with a growing alternative network of short and localised supply chains. The latter network will most likely be established in alliance with specialised suppliers that can deliver components and services, and have the capability to adapt resiliently to changes in market conditions.

Author: Vinay Piparsania

Week 15: Financial Crunch to Promote Alliances in Auto Industry

With most automakers remaining certain about their shift towards emerging mobility options, strategic partnerships and alliances can ensure their leap forward while maintaining a competitive advantage in these disruptive times.

Mobility options involving electric and autonomous vehicles require billions of dollars in investment. With automakers currently facing a severe financial crunch, the need for partnerships and alliances has become more relevant and urgent.

Below are some recent developments and measures taken by global automakers to ensure liquidity to manage their day-to-day operations:

- Daimler recently secured US$13 billion credit line from banks.

- Ford secured US$15 billion from existing credit lines and $8 billion from unsecured bonds.

- Volkswagen has announced losing US$2.2 billion per week due to plant shutdowns.

- French government will provide US$8 billion (EUR7-billion) bailout to PSA and Renault.

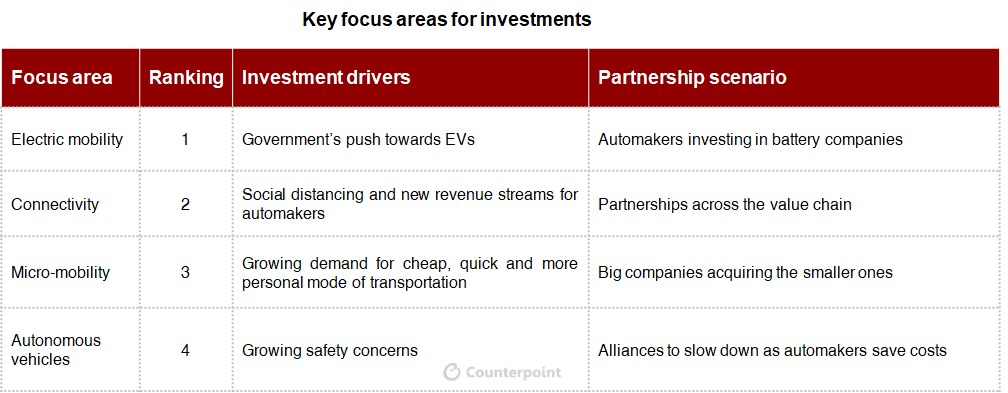

With the financial crunch leading to automakers and suppliers re-allocating capital funds to manage operations in the short term, Counterpoint expects investments to recover slowly post-COVID-19 and after operations become stable again. The table below ranks different strategic mobility opportunities in terms of their short-term investment potential, with comments on the probable partnership/alliance outcomes.

Electric cars

Investment drivers

With the automotive industry being a key GDP driver in many countries, governments will look at promoting EVs to meet their overall emission targets (Paris agreement) on the one hand while driving economic recovery and employment on the other.

Partnership scenario

A key area of partnerships includes EV batteries.

- Securing supplies: Automakers will need to ensure their battery supplies are secured by partnering with large-scale global battery companies like CATL and LG Chem.

- Saving R&D costs: Automakers will consider partnering with battery companies to develop energy storage technologies, saving or sharing costs.

Connectivity

Investment drivers

- Social distancing: Car buyers are preferring connectivity services like over-the-air (OTA) updates, predictive maintenance and touchless transactions, and looking to restrict their visits to service centres to maintain social distancing.

- New revenue avenues: OEMs are looking at value added connected services as an important area for generating additional revenues and shoring up profit margins amid declining vehicle sales.

Partnership scenario

There will be increasing partnerships across the ecosystem and supply chain — between automakers, telecom operators (to provide connectivity, subscription plans), TCU players (to provide the hardware) and software companies (to develop apps)

Shared mobility

Investment drivers

- Work-from-home options to employees are expected to become permanent for many companies moving forward, potentially leading to a surge in short-distance travel

- Amid the economic downturn, choices for last-mile and personal transportation will need to be economical. Hiring e-scooters, e-bikes and kickboards comes at a significantly lower cost when compared to owning a personal vehicle.

- Maintenance of social distancing is encouraging people to avoid public transport, boosting take-up of shared e-scooters and e-bikes.

Partnership scenario

- Acquisitions: There are more chances of acquisitions rather than partnerships in this market. With cashflows for small and medium companies remaining stressed, they are suitable targets for acquisition by big companies like Amazon at lower than the valuation price. Intel’s recent acquisition of Moovit, a mobility-as-a-service (MaaS) provider, for $900 million signals the possibility of similar acquisitions in the sector.

Autonomous vehicles

Investment drivers

- Growing safety concerns are expected to promote Level 1 and Level 2 autonomy features like adaptive cruise control and automatic emergency braking.

Partnership scenario

- There will be relatively fewer alliances (at least in the short term and compared to 2019) among stakeholders for advance autonomy (Level3+) as automakers try to invest in technologies with relatively faster RoI, and avoid cost on new technologies which are not proven and riskier to invest in.

Conclusion

While COVID-19 will delay immediate investments in new mobility, market drivers will continue to encourage investments in the long term.

Alliances and partnerships will become important tools for automakers to gain a competitive advantage. However, the nature of alliances will vary for each mobility type.

Author: Aman Madhok

Week 14: June Update – Global passenger vehicle demand to decline over 20% this year

COVID-19 continues to have a profound impact on the global passenger vehicle (PV) industry. As markets around the world move into H2, there are some varied signs of recovery visible, as well as of further turbulence ahead. Uncertainties remain, with COVID-19 infections rising in several countries of Asia and South America, and, most alarmingly, in the US.

Even as China was showing encouraging signs of a possible V-shaped recovery, June sales slipped significantly, indicating a bumpy ride ahead. The US industry too, despite having turned in some encouraging numbers in May, retreated last month. Europe, the UK and India remained sluggish and stuttering, with sales volumes expected to be under last year’s by over 25%, while South Korea remains a bright spot, tracking ahead on a year to date basis in June.

With the risk of further virus spread and preventive lockdowns remaining high over the rest of the year, Counterpoint analysts continue to remain cautious in holding to their earlier PV global sales forecast.

China

Based on recent numbers released by the China Passenger Car Association (CPCA), sales in China have significantly dropped in June, despite encouraging recovery trends demonstrated over May and April. Passenger vehicle sales came in around 1.68 million units in June, a 6.5% YoY decline. May sales had risen over 12% YoY to 2.1 million vehicles, and almost 4.5% YoY to 2 million vehicles in April.

The June decline is a setback for an industry expecting to see a rebound in demand with the pandemic having been brought under control in the country, and showrooms and retail markets reopening for business. Evidently, the auto industry’s long-term dependency on a broader economic recovery in China and on overcoming already established consumer mobility trends, such as preferring ride-hailing options and putting off purchase decisions, remains.

Sales of new-energy vehicles (NEVs), including electric cars, also continue to decline. NEV sales in June fell 35% YoY to 85,600 units, following a drop of 26% in May and 30% in April. After growing rapidly for several years, electric car sales have lost momentum, with the government rolling back subsidies in mid-2019 and prevailing lower oil prices making typical internal combustion engine (ICE)-powered vehicles more economical to operate. Electric vehicles (EVs), however, remain a priority for China and authorities are considering fresh stimulus measures to support their recovery.

Bucking the trend, Tesla accounted for nearly 23% share of electric car sales in June. The American company, which started production at its greenfield Shanghai factory at the beginning of the year, has rapidly achieved market leadership and boosted monthly EV registrations in China. Counterpoint analysts are monitoring Tesla’s rise in China and the impact its operations and popularity are having on other domestic EV manufacturers.

United States

In June, COVID-19 cases saw a spike in some key US states, including California, Texas and Florida, triggering fresh curbs on movement of citizens and resulting in some strong headwinds for the country’s PV sales. With more social restrictions and lockdowns likely to be introduced over the weeks ahead, recovery prospects for the US remain fragile.

Counterpoint analysts are holding to their earlier forecast of an over 24% annual decline for 2020, at around 13.4 million units.

On a positive note, Tesla’s market capitalisation now exceeds Toyota’s, making it the most valued carmaker in the world and underscoring its sustained global EV sales momentum over the pandemic period.

Europe

In Europe, we are beginning to see some improvement in vehicle markets, propped by a combination of pent-up demand and various government subsidy programmes encouraging drivers to trade in older cars for new ones. In France, car sales rose for the first time this year in June, recovering by 1.2% YoY to just under 234,000 units. Following France, Germany and Spain too have introduced similar incentives for their auto industries.

The UK car industry has also demonstrated signs of improvement in June, boosted by the reopening of more showrooms. According to reports of the Society of Motor Manufacturers and Traders (SMMT), June registrations fell 35% YoY to 145,377, an improvement over prior months when YoY demand fell by 89% in May, 97% in April and close to 45% in March. While car showrooms in England reopened at the beginning of June, dealers in Wales and Scotland were allowed to do so only from near the month end.

Notwithstanding the signs of a small rebound, Counterpoint analysts remain cautious. European and UK consumers are wary about buying high-ticket items like cars, given the uncertainty over the economy and their job security.

Rest of World

South Korea remains a bright spot in Asia, with domestic production and sales rebounding in June by over 41% YoY to 176,468 units.

In India, while leading automakers like Maruti Suzuki, Hyundai and Mahindra ramp up production and demonstrate incremental wholesale shipments month on month, sales remain a far distance from the pre-COVID-19 levels. June wholesale volumes for each of these automakers show an over 50% YoY decline. While PV production schedules for July may be higher, disruptions to the supply chain on account of COVID-19 induced restrictions and manpower availability continue to challenge their manufacturing stability. On the other hand, tractor and two-wheeler sales have seen a sharp recovery in June, led primarily by rising rural demand and resumption of movement of goods following progressive easing of lockdowns across the country.

Revised Global Automotive Outlook

While some varied signs of recovery have begun to emerge in June, Counterpoint Research remains cautious and is holding to its earlier global automotive sales outlook of around 72 million units for 2020, a 20.1% decline from 2019.

Author: Vinay Piparsania

Week 13: COVID-19 Impact on EVs

Overview

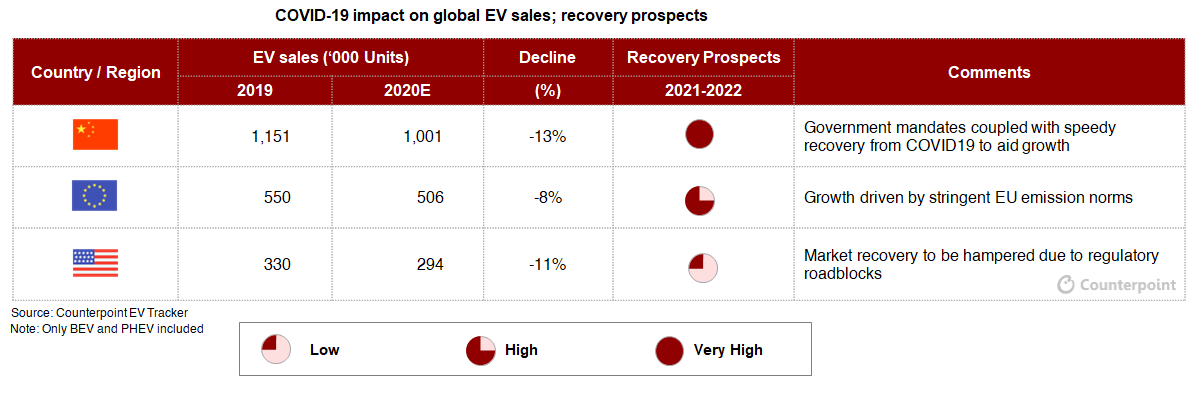

Counterpoint expects electric vehicles (EVs) to weather the pandemic storm better than the conventional vehicles due to the commitment of governments to meet their overall emission targets. The impact of the pandemic in 2020 will differ across regions. China will recover the fastest due to its control on pandemic spread and pro-EV policies. In longer term, the impact of the pandemic will be minimal and EV sales will be driven by government regulations and incentives. Despite slower recovery in Europe, the investment in the region is expected to remain strong in the long term, driven by strong regulatory tailwinds. Long-term demand in the US will be the lowest if the emission norms remain lenient and the oil prices remain low.

United States

The COVID-19 impact on the US EV market has been limited due to strong sales of Tesla during Q1 2020. Plant shutdowns during the March-May period have started making impact on all OEMs including Tesla, which reported 5% YoY decline in deliveries during Q2 2020.

The EV sales in the US will be hit hard by COVID-19 and see a slower growth in the coming years:

- In January 2020, the administration rejected GM’s and Tesla’s plea seeking extension of the $7,500 tax credit qualification to cover three times the initial 200,000-EV threshold per automaker. The government did not increase the threshold. On the contrary, it reduced the tax credit to $7,000.

- Protracted legal battles between Zero Emission Vehicle (ZEV) states and the central government will continue to adversely impact EV sales in the US, at least for the next couple of years. Cash-strapped automakers will be encouraged to invest in profitable vehicles like gasoline trucks and SUVs.

- Low crude oil prices (which fell to -US$37.6 in April) will encourage car buyers to stick to gas fuelled cars.

China

Chinese government has taken positive steps in 2020 to revive the demand for new-energy vehicles (NEVs). It is expected that the government will continue to support NEVs with sales mandates and subsidies driving the market.

- In April 2020, China scrapped vehicle purchase tax on NEVs, effective in 2021 and 2022, and broadened the scope of the exemptions to include all NEVs.

- The NEV subsidies were supposed to end this year. However, during the same month, the government announced to extend the subsides to 2022, with a slower phase-out pace.

NEV sales during the January-May period crossed 260,000 vehicles, declining 44% from last year. However, sales decline continues to drop with each passing month as the pent-up demand is released and business activities comes to normal. Counterpoint expects a strong H2 2020 for EV sales in the country compensating for the demand lost during H1 2020.

Europe

The European car sales increased around 90% during January-April 2020 compared to last year due to following reasons:

- 2020 is the target year for EU CO2 emission standards to limit average CO2 emissions per kilometre per new car sold

- Germany increased the EV subsidies in February, boosting demand in the region

- Italy’s move to introduce incentives worth €60 million in 2019 and €70 million in 2020 and 2021 started to have its impact on sales

The impact of the pandemic will be diluted during rest of the year as OEMs focus on meeting their emission targets. It is likely that the governments will respond to the pandemic by increasing subsidies and incentives for EVs to meet emission targets, boost economic growth and generate more jobs. The proposed US$22.6 billion (€20 billion) package for two years for clean vehicles, with 2 million electric and hydrogen vehicle charging stations to be installed by 2025, is a step in this direction.

Author: Aman Madhok

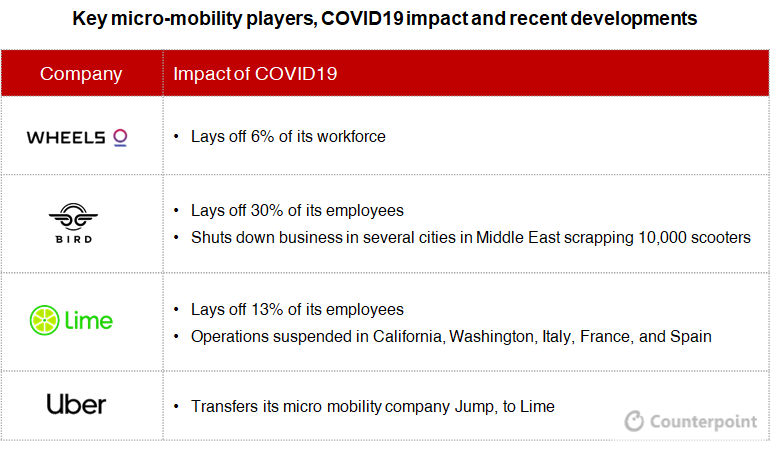

Week 12: Micro mobility – Silver linings amidst the pandemic?

Overview

Micro mobility globally has been severely impacted by COVID-19 with lockdowns resulting in reduced ridership. The road to recovery is a tough one, but Counterpoint believes micro-mobility will be the biggest beneficiary from COVID-19 among all forms of shared mobility.

Citizens and governments in many cities are becoming increasingly aware of the benefits of micro-mobility, and companies should prepare for coming opportunities to not only survive, but to grow over the long term.

Key indicators showing potential for rebound as lockdowns ease:

- Changing customer preferences – businesses are realising productivity is not an issue. In fact, it has increased in some cases as employees work from home. This is expected to become permanent for many companies moving forward, leading to a surge in short distance travel. People are more likely to choose quick and eco-friendly e-bikes and e-scooters as they travel short distances around their home rather than taking long commutes.

- Amidst the economic downturn, choices for last mile and personal transportation will need to be economical. E-scooters, e-bikes and kickboards are significantly cheaper than owning a car.

- Concerns around social distancing will encourage people to avoid public transport, boosting take up of shared e-scooters and e-bikes. In China, bike share operators like Hellobike, Mobike and Didi Chuxing are seeing good growth after easing of lockdowns, as people reduce dependence on public transport.

- Lockdowns have resulted in less pollution, increasing environmental consciousness amongst the general public. This is expected to benefit the sector in near future. Indeed, high pollution levels in many Chinese cities have boosted the profile of the sector, making bicycles and e-bikes an important mode of last mile transport.

Government support

To aid social distancing, governments are considering infrastructure investments to help the micro-mobility sector to grow.

- The UK government is urging people to avoid public transport and instead use private vehicles, bicycles, or walk. It has announced an initial £250m (US$306m) emergency active travel fund (the first stage of a £2bn investment commitment) for EVs, cycling and walking infrastructure. Buildout of E-scooter trails in the country will be brought forward to 2020 from 2021. Pop-up bike lanes, wider pavements and safe junctions will be a part of the fund. £10m (US$12.2m) from the fund will be committed to street EV charging infrastructure.

- Bogotá, Colombia has added 47 miles of cycling lanes to accommodate more riders and aid in social distancing. Cities such as Mexico City and London are benefiting from the current cycling infrastructure.

- Other cities have blocked some roads to traffic, providing more space for pedestrians and facilitate social distancing. For instance, Oakland, California has restricted traffic on 74 miles, or 10%, of its roads, helping pedestrians and cyclists keep at least six feet apart.

Green shoots

As lockdowns ease, some e-bike companies are already seeing an increase in demand.

- E-bike maker Vanmoof, which secured funding of $13.5m in May 2020, saw sales increasing 48% YoY during Feb-March period, and over 20% for the Jan-May period.

- UK-based foldable bike manufacturer Brompton announced its online sales increased five-fold since the launch of the ‘Direct To Home’ service from the start of April.

- E-bike sales in Germany have seen a significant increase from April with the easing of lockdowns, creating a shortage of e-bikes in many cities.

Challenges

- The global micro-mobility market recovery will likely start in 2021, or as we see stabilization in COVID-19 cases. A second wave of infections could delay the recovery further.

- Most micro-mobility companies are relatively small and localized start-ups, with many already seeing losses before the pandemic started. The market will see consolidation as cashflow continues to tighten. Intel’s recent acquisition of Moovit, a mobility-as-a-service (MaaS) provider, for US$900 million signals the possibility of similar acquisitions in the sector.

- E-bikes, e-scooters and kickboards are still illegal for travel on roads in many cities. Further, there is a lack of standardization for these types of vehicles.

Recommendations

- Governments can play a pivotal role in the adoption of micro-mobility. The recovery will vary from country to country depending on favorable government policies, subsidies and infrastructure development.

- Measures such as self-sanitizing handlebars, onboard sanitizers and periodic cleaning of vehicle fleets will become important to attract riders.

- Innovative schemes and discounts can help micro-mobility companies through the tough times. For instance, two-wheeler sharing company Bounce is offering its bikes on a weekly and monthly subscription basis.

Utilization of existing vehicle fleets into logistics and food delivery can open up new revenue streams for micro-mobility companies. For instance, two-wheeler sharing company Rapido is looking to earn 25% of its revenues from logistics moving forward.

Author: Aman Madhok

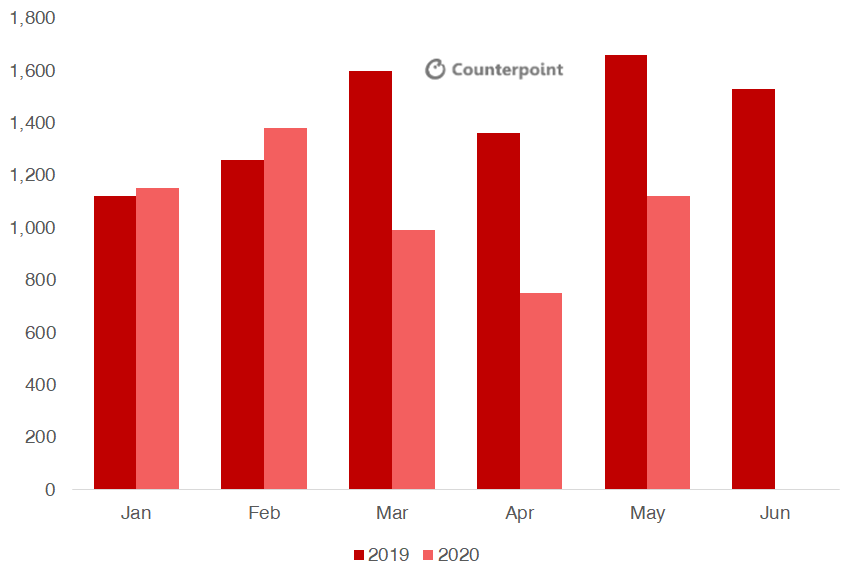

Week 11: US May sales – Is the worst over?

Actual passenger vehicle (PV) sales reported for the US in May suggest the domestic auto industry could be on its way to recovery.

Reported May sales for PVs and light trucks came in at around 1.1m units, down 33% YoY but an improvement over April and March’s respective 45% and 38% declines. Further, breaking the 1m monthly mark for the first time this year, May volumes showed significant improvement over the 350,000 units sold in April, with light trucks being a bright spot.

US auto sales on the rebound

May is traditionally a critical month for the US auto industry as it marks the beginning of the summer sales season. With almost all states having eased COVID-19 restrictions, most automakers in the country have reported sales rebounds during May.

Monthly sales declined over 30% YoY for General Motors, Ford, and FCA. Leading Korean carmaker Hyundai saw a 13% YoY decline, a 5% pt improvement from April. Honda saw a May YoY sales drop of 17%, with trucks performing much better than cars – down 10% and 25%, respectively. Toyota reported a YoY sales decline of 26%, May’s unit sales were almost double that of April, which fell 56% YoY.

It is possible April could be the low point in a possible V-shaped recovery, with states re-opening and dealerships returning in May. The month has shown significant sales improvement and recovery, highlighting pent-up demand. As well, extraordinary promotional offers by dealers and automakers alike have brought consumers back to showrooms and encouraged buying.

Counterpoint believes that May’s sales pace, while lower than last year, is indeed the start of recovery for the industry. Automakers are already scrambling to replenish inventories as customers return to showrooms. However, there is still a long road ahead, and we will continue to track the market over the coming weeks.

Production hiccups stalling assembly lines

As many states across the country eased shelter-in-place restrictions during the month, May also brought attempts by auto OEMS looking to return to normalcy with restarts at their assembly plants.

However, supply chain issues continued to plague production lines at major auto plants, as they faced problems from suppliers in Mexico. While most plants in the US and Canada restarted by mid-May, most manufacturers in Mexico had not resumed operations even by the end of the month. Given the inter-dependency of the North American automotive supply chain, most plants in the US continue to face parts shortages, resulting in sporadic production operations. It may still be a few months before we see some stability.

Counterpoint estimates prolonged plant/supplier shutdowns have resulted in the loss of nearly 3m units of vehicle production in H1. Anticipating slower line-speeds and reduced demand over Q3 and Q4, we expect full-year 2020 output losses to increase to over 3.5m units, a 22% decline from last year.

In any case, with automakers already concerned about record low inventories at dealerships, carmakers have been looking to continue working over normally planned shutdowns in summer.

Keen on riding the wave in customer demand, especially for light trucks, General Motors has called off its traditional two-week summer shutdown and will continue to produce vehicles at most of its North American plants.

Similarly, Ford Motor Company has shared that most of its US assembly plants will be reducing their annual summer shutdowns to one week.

As well, most other auto OEMs are considering deferring annual summer breaks to later in the year.

Sales recovery to hit headwinds?

The question going forward is whether recovery signs will continue into June and further out.

While recent trends suggest sales are showing steady gains and automotive manufacturing in North America is gradually coming back on stream, there is also the possibility of a resurgence of the virus bringing further economic headwinds.

However, Counterpoint continues to maintain its current outlook for the US auto PV and light trucks market at a base case estimate of almost 13.4m units in 2020, marking a 24% YoY contraction.

Exhibit 1: US Vehicle Sales,’000 units

Author: Vinay Piparsania

Week 10: Changing consumer behaviors and how mobility companies can adapt

The pandemic is affecting most sectors of the economy, especially shared and smart mobility operators. Public-transport usage in major cities has declined anywhere from 70 – 90% of normal loads, and operators are now required to follow strict protocols like requiring face coverings, temperature scans and limiting the number of riders in trains and buses to ensure social distancing.

Similarly, ride-hailing mobility usage has plummeted dramatically, with several players suspending services during lockdowns. In the US, demand for Uber and Lyft fell by over 80% in April from pre-COVID levels.

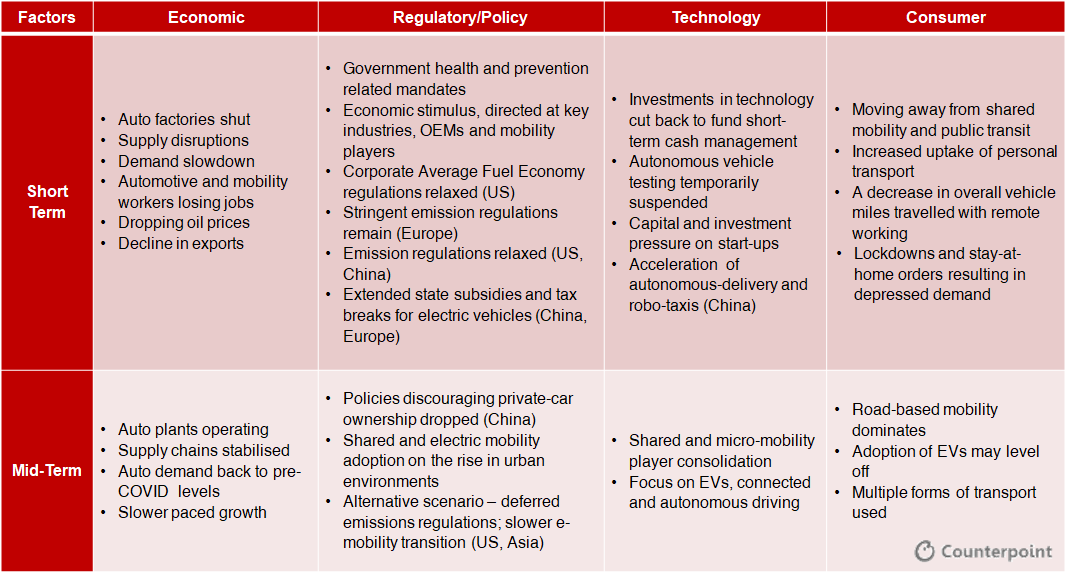

Over the long term, the outbreak will have lasting impacts on shared mobility as the pandemic alters the economic, regulatory, and technology environment, as well as changing consumer behaviour.

Changes in consumer behavior and preferences

Mobility is an essential aspect of our lives, but how we get around in the future could be significantly different in the post-COVID world. Social distancing is the most significant driver of change in this new environment, with people rethinking their transport modes to avoid the risk of infection. Recent trends in China’s major cities are demonstrating that as bus and subway ridership drops, private cars, walking, and biking are gaining in popularity.

Personal vehicle use may be the winner in the short term, and app-based ride-hailing aggregators are seeing a dramatic decrease in consumers using their services as remote working becomes the norm.

Further demands are being made on share-car drivers and their companies to take responsibility for keeping vehicles clean and virus free. To adapt, mobility industry players are adjusting their tactics, with leading companies focusing on various strategies.

Lyft

Lyft, which announced cuts and furloughs affecting hundreds in May, stated that rides on its platform in the US reached only 25% of pre-COVID levels during the month, with consumers slowly coming back in cities where lockdown restrictions were eased. Lyft drivers are now required to self-certify within their app of wearing a facemask before they are allowed to pick up passengers.

Uber

While the global number for June trip requests are picking up as several countries ease restrictions, rides are still significantly below last year’s levels. In an attempt to improve profitability, Uber has remained focused on its core businesses of ride-hailing and food delivery, and also announced cuts to its workforce. Uber also introduced a new feature requiring drivers to take a selfie of themselves wearing a facemask before logging onto the company’s network. Uber has also been providing disinfectant sprays to drivers, encouraging them to sanitize their cars regularly.

Didi Chuxing

With cities in China now officially re-opened for business, Didi Chuxing, the country’s largest ride-hailing app, is seeing ride-sharing demand coming back to levels similar to last year. Since May, Didi has been using AI technology to authenticate that its driver-partners are wearing face masks.

Diverse regulatory and policy responses across regions

The current crisis is helping some regions move more quickly towards sustainable mobility, while others are looking to defer or relax regulatory mandates to support depressed automotive industries.

In some markets, incentives such as cash for turning in old cars is driving sustainability through replacement and also encouraging adoption of electric vehicles (EV). In other regions, like the US and China in particular, regulators have considered relaxing emission targets in support of automakers.

Chinese regulators are also relaxing, at least for now, policies limiting personal vehicle ownership in order to facilitate social distancing. Many governments are also showing interest in dedicating space for pedestrians and cyclists, while some cities like New York are looking to close some streets to vehicular traffic.

Technology development

Over the short to medium term, the pandemic could delay the development of advanced technologies, such as autonomous driving, as automakers divert research budgets to fund immediate cash requirements. Similarly, investments in micro-mobility and shared-mobility start-ups are expected to fall and could drive market consolidation.

The impact of COVID-19 on EV development will differ across regions. In China, we expect post-COVID EV sales to rebound, with continued investment in development. In Europe, while ramp-up of EVs may be delayed with historically low oil prices, stringent environmental regulatory pressures could remain a counter-balance. In the US, we could see EV demand stagnate should federal emissions regulations be eased and oil prices remain subdued.

Over the long term, however, autonomous vehicles, micro-mobility solutions and other technologies that support physical distancing will benefit. We believe that as the initial crisis subsides, customer demand for these solutions could soar.

How can mobility companies cope?

Even before the pandemic, mobility and automotive start-ups were suffering from slowing growth in major economies. Battered by lockdowns and movement restrictions, ride-hailers around the world have had to resort to cutting jobs and slashing costs.

Looking ahead as the pandemic gradually comes under control, mobility companies will need to look at developing detailed plans to scale up operations, not only focusing on where, but how. A portfolio review aiming to rationalise services can help focus on profitable operations and decide on which technologies are to be prioritised, so to emerge from the crisis leaner and stronger.

Conclusion

Counterpoint believes recent consumer behaviour changes in the mobility space will be temporary, and shared-mobility solutions, including public transit, will rebound. Micro mobility and last-mile solutions, too, will eventually recover, as cleaning and disinfection protocols are practised, with status updated on ride-hailing apps.

Now more than ever, it has become imperative for automakers and mobility operators to review their long-term strategy.

Exhibit 1: COVID-19 Impact to Global Automotive and Shared Mobility Industry

Author: Vinay Piparsania

Week 9: Poised for a rebound? May’s mixed signals

As the effects of the pandemic are being brought under control, we are seeing gradual automotive sector recovery, though at varied rates.

With most parts of the world easing lockdowns in May, auto sales have begun to show some signs of improving. Prospects for China, having reopened earlier than most, and the US are looking more positive than for Europe.

In the short term, the global automotive industry appears to be poised for a rebound as manufacturers replenish dealer inventories and meet pent-up demand, especially with many consumers expected to take efforts to avoid public transport and ride-sharing.

Longer-term, however, Counterpoint sees a more gradual recovery, with dampened vehicle sales from Q1 carrying over into Q2. Supply-side issues will also cause problems, with stuttering production schedules from broken supply chains, financially stressed suppliers, and delayed new model launches limiting supply.

With some leading indicators now visible, we have decided to maintain our current 2020 PV forecasts. However, key risk factors of a virus resurgence remain high for some locations, with the possibility of markets going into lockdown again.

Below is our latest outlook, incorporating May sales updates from key global markets.

China

The first country to be impacted by the virus outbreak, China has been quick to recover from the pandemic, and PV sales are almost back to pre-coronavirus levels of growth. Largely on account of the automotive industry’s effective restart in March, sales and production activity approached normal levels in April, with PV sales up 4.4% YoY to 2.1m units. May saw further improvement, with sales rising 12% YoY to 2.1m vehicles.

Pent-up demand drove steady deliveries in April. This was further supported by government subsidies and intensive promotions and discounts offered by dealers. The momentum continued into May, raising our overall expectations for Q2.

However, domestic and global headwinds remain, and the market still faces a high level of economic uncertainty. Consumer confidence is fragile, with fear of unemployment and income loss dampening high ticket, discretionary purchases.

As a sustained, comprehensive recovery is still to be established, prospects for H2 remain cloudy and we maintain our current forecasts.

US

May sales are estimated at around 1.1m PVs, down 30% YoY, but an improvement to April and March’s respective declines of 45% and 38%. Easing of restrictions across most of the country helped May pass the one million mark.

Throughout the lockdowns, however, the market did demonstrate some resilience, with significant commercial activity continuing as vehicle sales were categorised an ‘essential service’ by many states.

While American retail consumers are coming out again to look at cars and trucks, facilitated by digital retail tools and appealing discount offers, fleet and commercial category buyers, particularly those in rental cars, are not. This is worrying as new vehicle sales to rental car companies accounted for about 10% of the overall market, or 1.7m vehicles, last year. Bankruptcy filings of Hertz and its parent company Advantage Rent A Car in the last week of May will likely weigh down US auto sales.

We maintain our current outlook for the US, with a 24% YoY contraction expected in 2020.

Europe and the UK

European car sales picked up slightly in May after a disastrous April. In Spain, May sales dropped over 72% to 34,000 units, and to almost half previous year totals in France, Italy and Germany, which saw sales of 96,000, 100,000, and 168,000 units respectively, as partial lockdowns remained. Overall, YoY sales for Western Europe fell over 57% in May, to 556,000 units.

For the UK, new car registrations were down 89% YoY in May, with 20,200 cars registered last month. Despite the drop, the figure marks an almost five times increase over new car registrations in April, when only 4,300 cars were sold. The Tesla Model 3 topped the UK new car sales chart for the second month running, with 850 units delivered, making up nearly 5% of all registrations.

With around half a million new cars registered since the beginning of the year, the overall UK market has halved in the first five months of 2020, compared to almost one million units registered during the same period last year. While showrooms in England have reopened after two months, dealerships in Scotland, Wales, and Northern Ireland are still shut.

Reopening’s have helped sales in Germany, with May sales falling by 50% compared to over 60% in April.

As we look ahead, Counterpoint is paying particular attention to any government announcements around fiscal policy or economic relief programs such as that planned for France and Germany, which are looking to lower VAT. While details will vary by country, recent announcements imply modest levels of incentives can be expected.

Even with some signs of improvement in May, the industry remains in crisis, with various stages of lockdowns expected for some time. Our outlook for Europe remains unchanged – a 26% contraction expected in 2020, with the possibility of a gradual recovery in H2 2020 as consumer sentiment improves with the easing of lockdowns.

India

After zero sales in April, preliminary shipment data for May suggests only 37,000 units were sent to dealerships, an 85% decline YoY, as the country started to open up gradually during the month.

With auto OEMs and dealerships estimated to be holding nearly 300,000 units of inventory – about two month’s stock based on current projected retailing rates – wholesale shipments over the next few months are expected to be difficult.

Overall consumer sentiment in the country remains weak, mostly because of the economic fallout of a complete nationwide lockdown lasting 50 days, depressing GDP forecasts, and increased caution around car loans. For any significant recovery to happen this year, it is critical that automakers and dealers have operations and consumer offers fully in place as the festive sales season commences during the last quarter of the year.

Our India sales forecast remains unchanged. Our base case outlook sees YoY passenger vehicles declining by 25% to around 2.1m units.

Japan

While having been a relative bright spot so far, the Japanese market worsened in May. Sales dropped, nearly 55% YoY to 218,285 vehicles, compared with a 29% YoY decline in April.

Consumer sentiment remained depressed, with expectations of an economic downturn curbing big ticket purchases. Also, the government’s declaration of a state of emergency and stay-at-home advisory, which ran into the Golden Week holiday in late April to early May, severely impacted sales, which normally spike during the annual holiday.

While overall economic activity shows some positive signs of recovery since lifting of restrictions in May, our outlook remains unchanged.

Revised Global Automotive Outlook

While varied signs of recovery began to show in May, Counterpoint Research remains cautious and we leave our earlier global automotive sales outlook unchanged at around 72m units for 2020, a 20.1% decline from 2019.

Exhibit 1: Global Automotive Sales (M units)

Note: The nature of the current global health crisis means we cannot rule out further revisions to the global 2020 automotive forecast.

Author: Vinay Piparsania

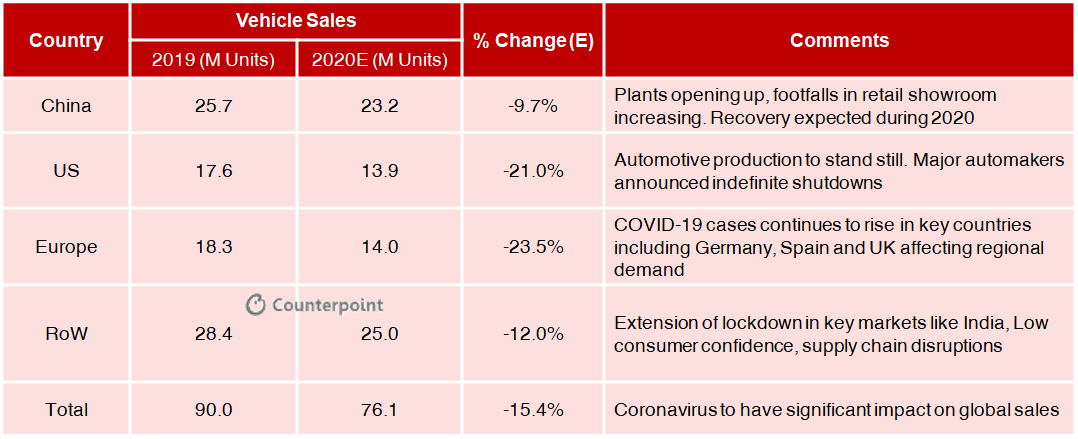

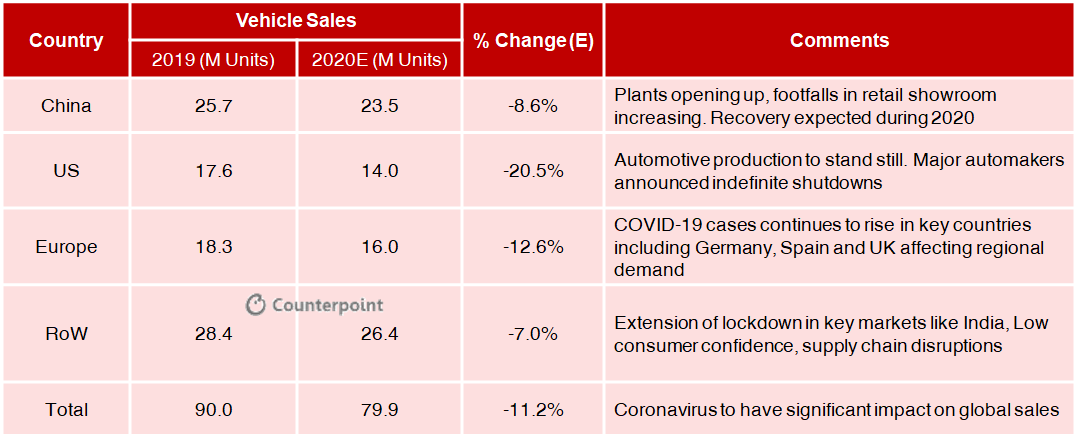

Week 8: India’s Auto Industry to decline by at least 25% in all categories in 2020

India’s automobile industry, the fourth largest globally by volume, is headed for another year of significant declines as extended lockdowns impact production and consumer demand. Sales volumes of passenger and commercial vehicles are projected to drop to levels not seen in over a decade.

The storm continues

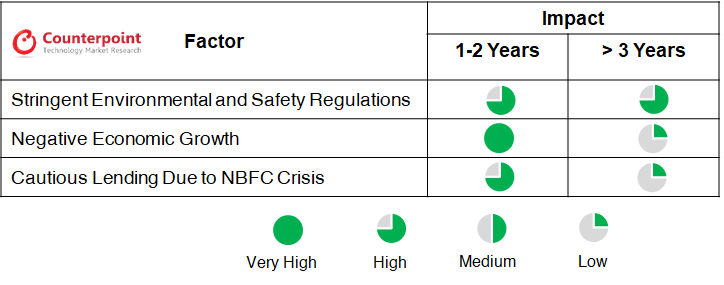

At the beginning of the year, the auto sector was already suffering in the midst of a challenging economy. Compounding this, more stringent environmental and safety regulations, the growing popularity of shared mobility platforms and cautious lending by banks and non-banking financial companies (NBFCs) negatively impacted vehicle sales. COVID-19 is now making the situation far worse.

Based on data reported by the Society of Indian Automobile Manufacturers (SIAM), March passenger vehicle sales declined 51% YoY to 143,014 units. Sales of two-wheelers fell 40% to 866,849 units, and commercial vehicles declined 88% to 13,027 units. With a nationwide lockdown in effect from the last week of March, the industry saw zero production and sales of new vehicles in April.

Factories and dealerships struggle to resume operations

While automakers began partial operations in May, it has been an uphill struggle. Openings were allowed only after receiving due approvals from respective state authorities, and conditional to following safety protocols such as body temperature scanning, social distancing and ensuring high standards of sanitization.

Shutting down operations was far easier than reopening factories as companies need to manage complex synchronization issues. The resumption of operations requires OEMs to coordinate with hundreds of local and global suppliers, logistics partners and thousands of employees. The biggest challenges come from not having enough workers willing to come back and sufficient and continuous parts supply. It is likely plants across the country will function with a skeleton staff at least until July.

Slow dealership re-openings are another problem, with almost all vehicle sales delivered through them – online sales are a rarity and still under development. As of the last week of May, only 3,500 dealerships were operational around the country, representing 20% of the total network. And amongst these, half were operating only their service departments and not showrooms.

The sharp contraction in sales will also lead to a decline in average manufacturing capacity utilization. For the PV segment, effective annual capacity utilization is projected to drop down to as low as 45%, from 60% a year ago. Two-wheelers and commercial vehicles will drop to below 50% and 35%, respectively, from 65% and 51% a year ago.

Demand outlook for 2020

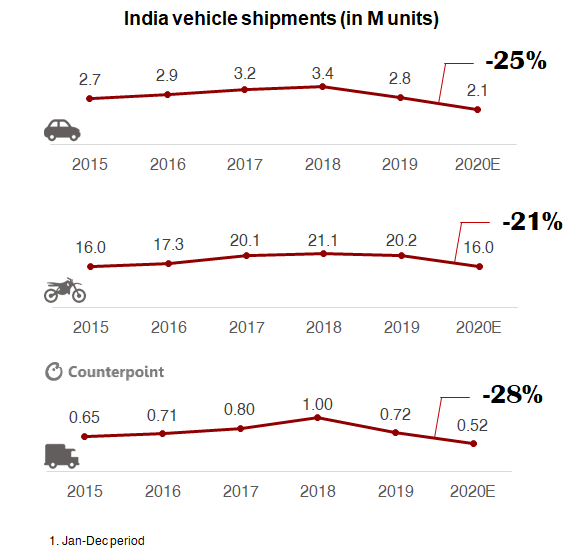

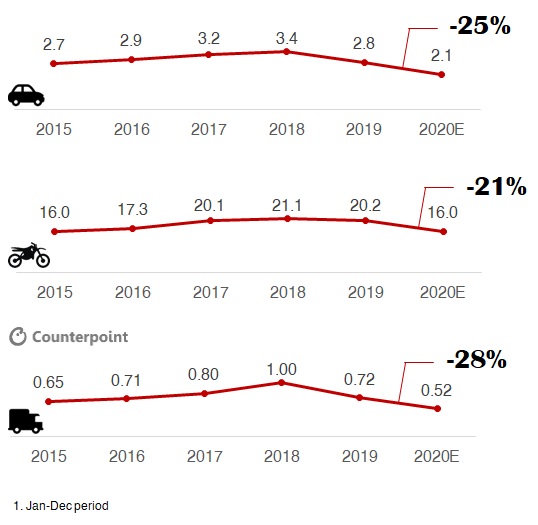

The lack of government policy intervention for the automotive sector in this year’s national budget and also recent fiscal stimulus packages combined with a lack of visibility around when social and economic demand conditions will get back to normal has resulted in Counterpoint revising our 2020 forecasts. Our base case outlook sees YoY passenger vehicles, two-wheelers, and commercial vehicles declining by 25%, 21% and 28%, respectively. CV sales in particular, have been languishing under the impact of a new axle load norms, and is unlikely to show much recovery this year with freight demand projected to remain low.

Recovery timing

Demand recovery can only be expected around the festive season in the last quarter of the year. With growing consumer preference for cheaper, personal transport, two-wheelers – motorcycles in particular, with their higher rural share – will likely be the first category to see a rebound. Should the government develop scrappage schemes and lower interest rates for vehicle loans, along with reduction in sales and road taxes, as seen across SE Asia, these interventions could accelerate recovery.

Despite the above challenges, we remain positive longer term in view of India’s comparatively low vehicle penetration – 110 two-wheelers and 32 cars per 1,000 – Australia has 740, Japan has 591 and China has 164 vehicles per 1,000 individuals. We expect recovery post-2022, helped by improvement in non-banking financial institutions and the overall economy. Combined with a young population, rapid improvements in road infrastructure, growth in rural demand and possible introduction of entry-level passenger cars, this could significantly boost consumer demand.

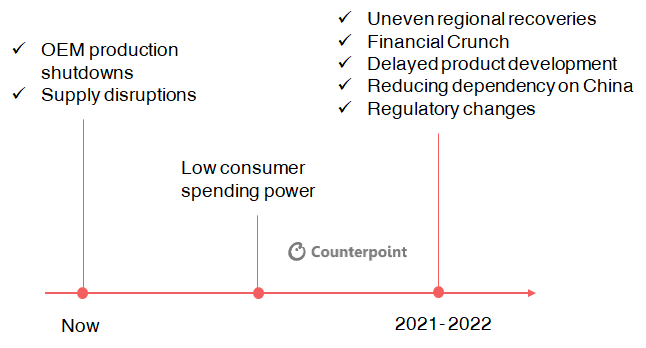

Exhibit 1: Key Factors Affecting the Market

Exhibit 2: India Vehicle Shipments1 (in Million Units)

Note: The nature of the current global health crisis means we cannot rule out further revisions to the global 2020 automotive forecast.

Author: Vinay Piparsania

Week 7: Southeast Asia Pressure Points

As the world continues to deal with COVID-19, economies are moving into recession. The automotive sector, with its large-scale production and tightly interconnected global supply chain, remains the worst impacted.

This week we focus on the impact to Southeast Asia, with ASEAN representing the fifth-largest auto market cluster in the world.

Lockdown measures introduced mid-March

Like many others, most ASEAN countries underestimated the risk of outbreak at the start of the year, with governments doubtful on it becoming a pandemic. Remaining tentative on diverting resources to public health, most ASEAN countries waited, introducing lockdown measures only around mid-March. As a result, key economic sectors in the region remained, for the most part, unaffected by the outbreak before this time – this included international travel, tourism, and export dependant businesses.

However, as the crisis erupted and lockdowns ensued, millions across the region rapidly began losing jobs as business came to a standstill. As immediate countermeasures, central banks across the region introduced rate cuts and easier lending terms to ensure liquidity. Governments also announced fiscal support measures including direct disbursement, soft loans, and tax cuts to mitigate the impact of the potential economic crisis.

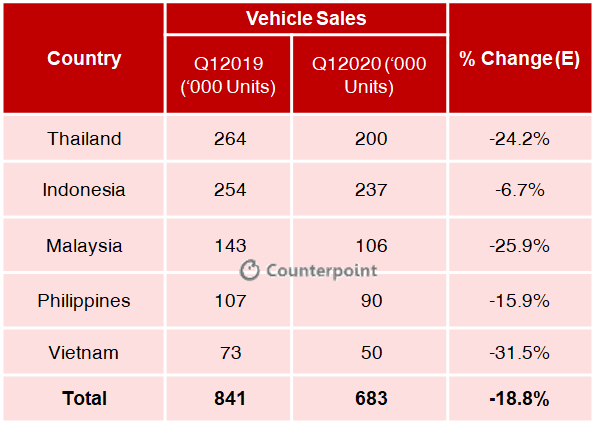

The auto sector has been hit hard, with overall Q1 vehicle sales in ASEAN5 (Indonesia, Malaysia, Philippines, Thailand, and Vietnam) falling to 683,000 – levels not seen in nearly a decade.

Declines for the month of March are the most revealing, with new vehicle sales plummeting around 40% YoY across ASEAN, and auto OEMs selling only 197,000 vehicles – this compared to 328,000 a year earlier. We expect April to be worse, with auto production remaining shut across the region last month and economic damage possibly worse than the 1998 Asian financial crisis.

Significant revisions to our Indonesia, Thailand, and Malaysia Automotive Outlook

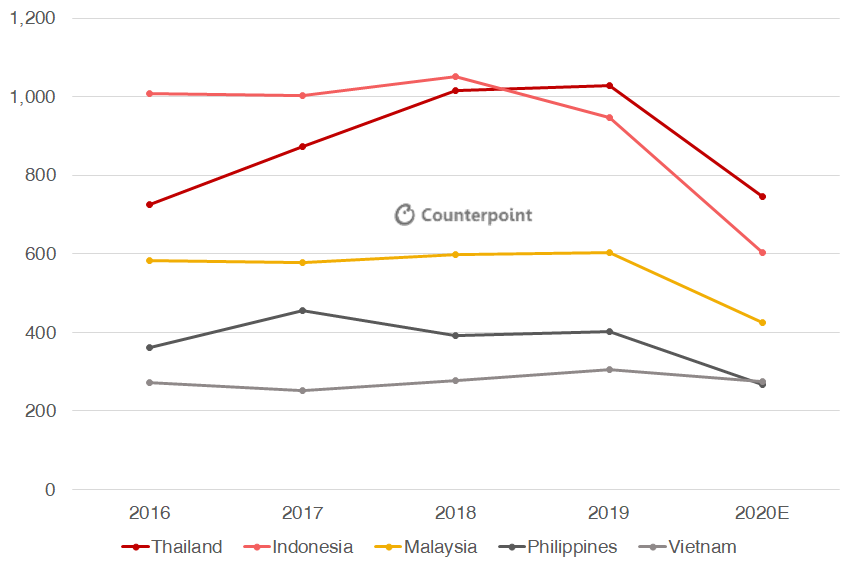

Economic growth in the region was already slowing down due to US-China trade tensions, and lockdowns have only exacerbated the situation – especially in Thailand and Malaysia. The extent and duration of distancing measures have been severe, and we have reviewed our FY 2020 outlook in this updated context.

Indonesia

In Indonesia, SE Asia’s largest auto market by volume, vehicle sales saw a comparatively moderate Q1 decline of 7% YoY to 237,000 units, with negative lockdown effects mitigated by a mid-March rollout. Though skeptical early on, the government eventually announced a partial lockdown on March 18, allowing only essential businesses such as food, healthcare, banking, and utilities to operate; as a result, vehicle sales for the month dropped 15% YoY to 77,000 vehicles.

With the full effect of shutdowns to be felt in the weeks ahead, we project steeper YoY vehicle declines from April onwards. And with a recession imminent, Counterpoint estimates this year’s auto demand to fall 36% to 603,000 units.

Thailand