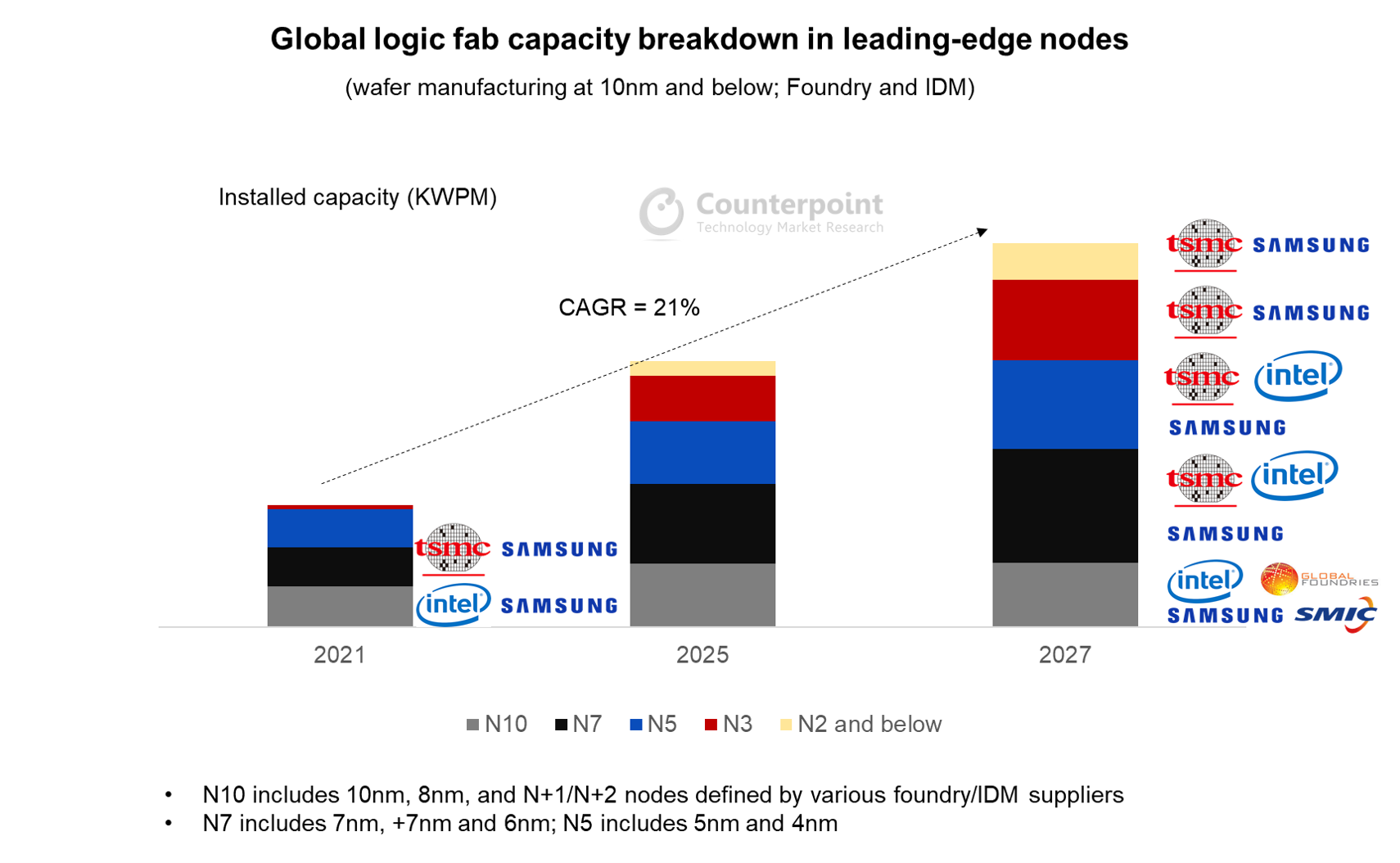

- Counterpoint estimates a 21% increase (CAGR) in the average annual wafer capacity of leading-edge logic (non-memory) IC nodes (defined by 10nm and below) for worldwide foundries and IDMs during 2021-2027.

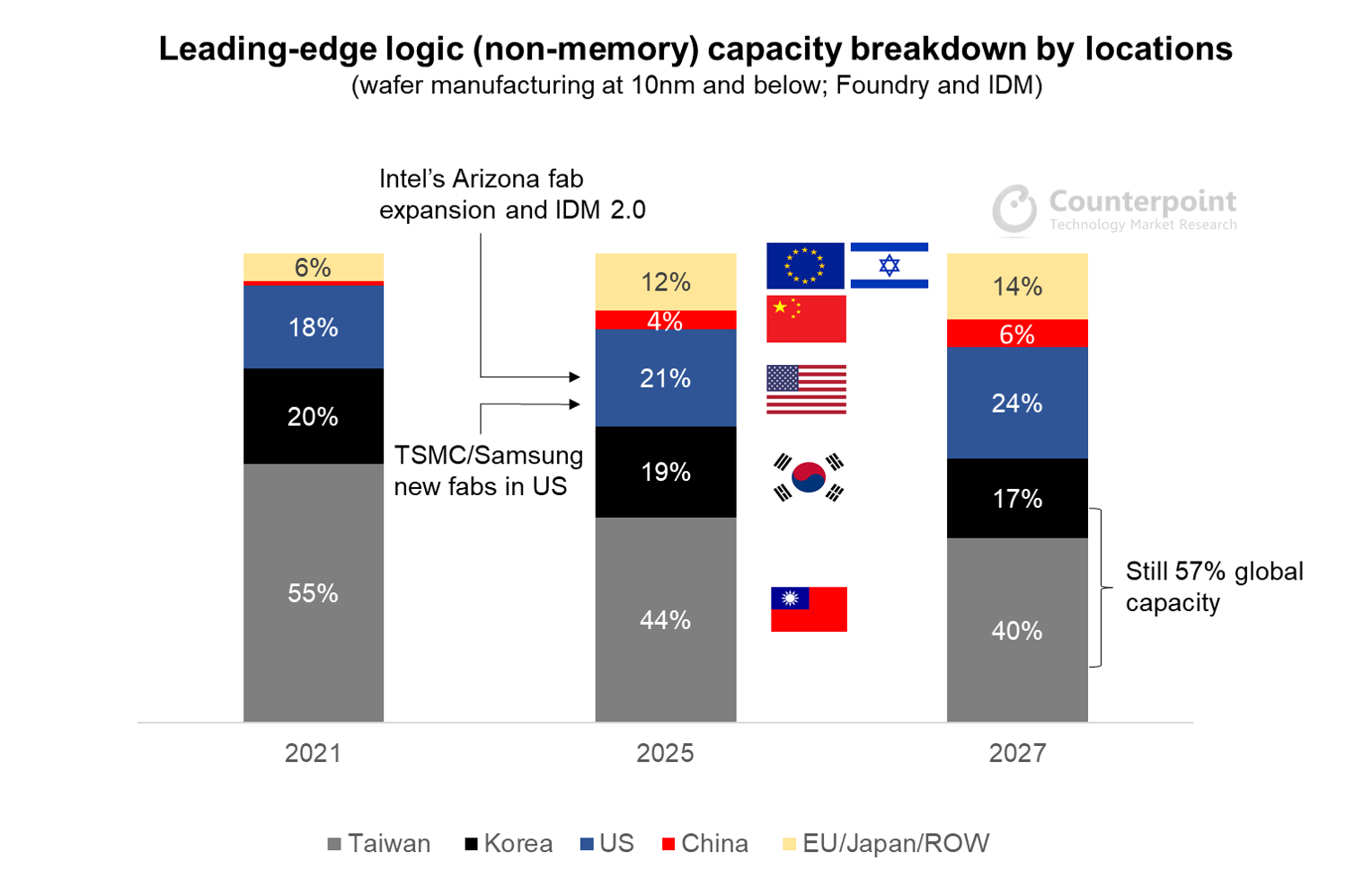

- The US is expected to increase its capacity share from 18% to 24% between 2021 and 2027, compared to Taiwan’s 40%, supported by the US government’s funding under the CHIPS for America Act.

- From a regional perspective, Taiwan and South Korea combined are projected to account for a majority (57%) of capacity globally in 2027. China will be far behind at 6% after 3-5 years from now, due to lack of manufacturing equipment on intensified levels of geopolitical competitions.

- From a demand perspective, the leading-edge monthly wafer consumption for each long/big node (such as 14/12nm and 7/6nm) is about 250,000-270,000 in 2021. We estimate this to increase to 300,000-320,000 by 2025, driven by mainstream 5G smartphones and data centre processors besides longer production lead time. We do not see major oversupply risks after three years despite massive capacity expansion plans.

In this note, we deal with two most asked questions from supply chains amid a global IC chipset shortage and new capacity expansion announcements during the past 3-4 months:

- Will the global logic IC fab landscape get altered in terms of geographical locations after the massive capex increase planned by industry leaders is implemented?

- Will we encounter capacity oversupply after these new leading-edge fabs enter mass production?

The questions raised above could be looked at in the context of TSMC’s statement in March which warned of possible double-booking of wafer orders. The bullwhip effect could eventually lead to an inflection point of demand/supply reverse in the next few months. Furthermore, the political uncertainties and climate concerns surrounding Taiwan raise the risk of a global industrial disruption due to the concentration of global chip manufacturing in the country.

Most of the capex plans of industry leaders, including TSMC, Samsung and Intel, aim to build greenfield fabs in the next few years. The leading-edge nodes are the focus of their capacity expansion plans, which start at $15-20 billion as the minimum investment to reach the production scale.

Fab capacity by regions

Counterpoint’s Foundry Service data provides current capacity/production shares across all regions. In the light of recent developments, we update our forecast for a complete analysis of the logic (non-memory) IC industry. For 2021, we see 55% of wafer capacity below 10nm (including all current nodes in N10, N7, N5 and N3/N2 in the future) located in Taiwan, followed by South Korea (20%) and the US (18%). TSMC and Samsung Foundry (LSI) represent all the lines in Taiwan and South Korea respectively, while Intel is the major one in the US to ramp up its 10nm CPU lines during the two years.

Moving ahead, the total built-in wafer capacity in the leading-edge nodes in 2025 is estimated to increase by more than two times, primarily at the companies based in Taiwan (TSMC’s 3/2nm), South Korea and the US, when Intel, TSMC and (likely) Samsung start to ramp up their new facilities in Arizona and Texas. We believe that under the CHIPS for America Act, both local and foreign players will be pushed to follow production schedules to avail government support. Therefore, we forecast that the US’ capacity share will get boosted to 21%, surpassing South Korea’s, with the majority of nodes in the US on 5nm and in Intel on 7nm. We also notice that Intel’s expanded overseas fab production, including in Ireland and Israel, will help the EMEA region grow capacity shares in leading-edge technologies. However, our forecast excludes the possibility of Europe introducing subsidies to lure investments in new fabs.

Predicting the regional shift in the long term (2027) based on current visibility, TSMC is likely to add more phases in Arizona after the initial 20Kwpm (wafer per month) investment to reach the mega fab scales it has in Taiwan. Intel too may take its US capacity more seriously during the period. However, compared to the large global expansion cycle forecast for 2021-2025, there will be a modest addition in the capacity during 2025-2027, with Taiwan, South Korea and the US accounting for 40%, 17% and 24% shares respectively.

Predicting the regional shift in the long term (2027) based on current visibility, TSMC is likely to add more phases in Arizona after the initial 20Kwpm (wafer per month) investment to reach the mega fab scales it has in Taiwan. Intel too may take its US capacity more seriously during the period. However, compared to the large global expansion cycle forecast for 2021-2025, there will be a modest addition in the capacity during 2025-2027, with Taiwan, South Korea and the US accounting for 40%, 17% and 24% shares respectively.

In contrast, China is forecast to take just 5-6% share in leading-edge fabs in the next 3-5 years. We expect the import restrictions on equipment for 10nm nodes (and below) to persist for a considerable period, forcing local foundry/IDM makers like SMIC to increase capacities in matured nodes.

Wafer demand-supply outlook for advanced nodes

We estimate a 21% increase (CAGR) in the average annual wafer capacity of leading-edge logic (non-memory) IC nodes (defined by 10nm and below) for worldwide foundries and IDMs during 2021-2027.

Our forecast indicates an aggressive build-up in capacity after a multi-year under-investment which became the root cause of the current IC component crunch. We estimate that a capacity of 160Kwpm (wafer per month) at 7nm and 100Kwpm at 5nm will be added globally in 2025. It includes Intel’s expanded 7nm in its global fabs, and TSMC and Samsung’s new fabs in the US.

Our forecast indicates an aggressive build-up in capacity after a multi-year under-investment which became the root cause of the current IC component crunch. We estimate that a capacity of 160Kwpm (wafer per month) at 7nm and 100Kwpm at 5nm will be added globally in 2025. It includes Intel’s expanded 7nm in its global fabs, and TSMC and Samsung’s new fabs in the US.

From a demand perspective, the mega trend of digital transformation will drive more new applications in mainstream 5G smartphones, data centre processors and autonomous driving (L4/5) in the next few years. In 2021, the total monthly wafer demand of each big/long node generation, such as 16/14nm and 7/6nm in logic IC fabs, is expected to be 250,000-270,000. In 2025, the monthly wafer demand is projected to increase to 300,000-320,000 for each leading-edge node. We expect the global wafer demand and supply for N5 and N7 nodes to be more balanced in 2025, after the massive new line constructions in the next 2-3 years. However, we do not expect any oversupply situation without a serious decline in global semiconductor demand.