Qualcomm Revenue Declines on Demand Weakness Across Handsets, IoT products

- Automotive and IoT segments were the bright spots and remained on a growth trajectory.

- H1 2023 will see inventory correction with some demand coming back in H2 2023.

- The current weakness in the semiconductor industry is more cyclical than structural.

Sources: Qualcomm, Counterpoint Semiconductor Tracker

October-December quarter analysis

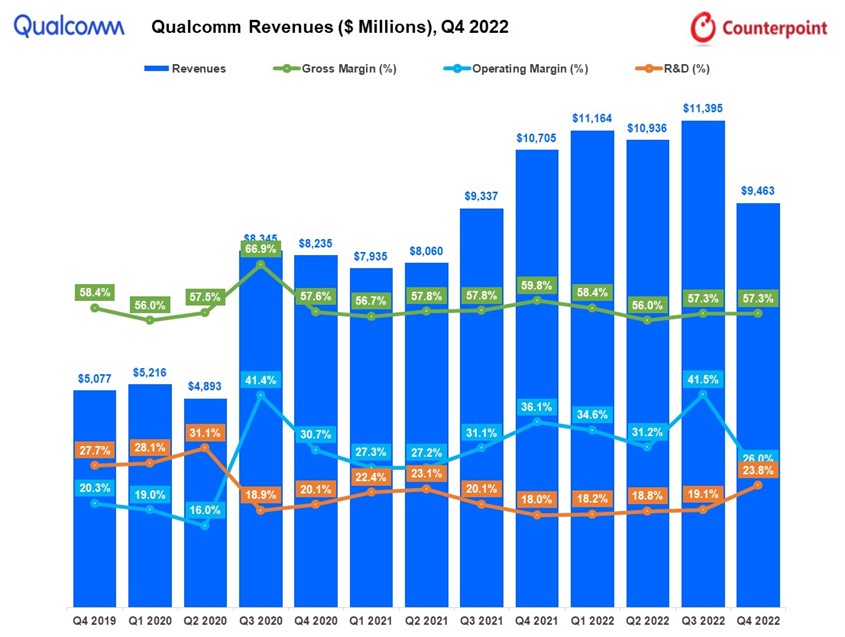

- In Q4 2022, Qualcomm’s revenues declined 12% YoY to reach $9.5 billion.

- QCT’s chipset revenues declined 11% YoY to $7.9 billion and QTL’s licensing revenues declined 16% to $1.5 billion due to weak handset sales.

- Within QCT, handset revenues declined 18% YoY to $5.7 billion. From Q4 onwards, RFFE revenues are being accounted for within each sub-segment. Qualcomm’s share in the Samsung Galaxy S23 series has grown from 75% to 100%. Overall, the higher inventory is affecting the handset business revenue.

- IoT revenues grew in single digits (7%) because of Edge Networking from the Wi-Fi access points and gateway routers.

- The automotive segment grew 58% annually to $456 million driven by the Snapdragon digital chassis.

- According to our RFFE report, Qualcomm’s RFFE revenues declined 18% YoY in Q4 2022. Handsets captured a dominant share in RFFE revenues. Qualcomm, which is already a leader in smartphone RFFE, has so far designed a win pipeline of over $900 million in the automotive segment and $405 million in revenues in the IoT segment.

Outlook

- According to the Counterpoint Market Outlook service, the smartphone market will be flat YoY in 2023. H1 2023 will see inventory correction while some demand will come back in H2 2023. We forecast excess smartphone AP/SoC inventory to return to normal levels by the end of H2 2023.

- FWA continues to have a big potential in driving IoT revenues, aided by both Sub-6GHz and mmWave. In India, Jio has publicly stated it will cover 100 million homes. Qualcomm is an investor in Jio and will gain from the modem and Wi-Fi-based content in 5G FWA.

- In 2021, Qualcomm acquired NUVIA, which enables custom CPU and design. Qualcomm has developed custom Oryon CPUs on ARM. This will further drive growth. We expect Arm-based laptops to have a 25% market share in five years.

- Further migration to Wi-Fi 6/6E, Wi-Fi 7, mesh networks and smart utility meters, trackers, e-mobility, parking meters, home automation and security, and other location-based solutions in the industrial sector is a key revenue driver.

- Qualcomm guided 2023 revenues in the range of $8.7 billion to $9.5 billion and non-GAAP EPS of $2.05 to $2.25. Their midpoint guidance includes an assumption of lower-end market demand and continued drawdown of channel.

Receive our insightful weekly newsletter and stay ahead of the competition.

Author

Parv Sharma

Parv is a Senior Analyst with Counterpoint Technology Market Research based out of Gurgaon, India. He has over 10 years of experience at Counterpoint in market research and strategic consulting across the global technology and telecom sectors. He tracks the global semiconductor ecosystem, with a focus on HPC and data center compute, server CPUs, and AI infrastructure — covering competitive dynamics across Intel, AMD, Arm, Nvidia, and hyperscaler custom silicon. His research also spans the smartphone semiconductor ecosystem — including the Application Processor (AP)/SoC market, foundry, node and manufacturing technology, the RFFE ecosystem and value chain, and smartphone Bill of Materials (BoM) analysis — as well as the Automotive and Connected Car value chain. He leads a team driving data analysis and insights and contributes regularly to media coverage on semiconductors and AI infrastructure.