Indonesian Smartphone Shipments Reached Record Volumes During Q2 2018

Smartphone Market Grew 25% annually; Xiaomi became the second largest brand for the first time ever

New Delhi, Hong Kong, Seoul, London, Beijing, San Diego, Buenos Aires – August 17th, 2018

- Indonesia smartphone shipments grew 25% annually and 5% sequentially during Q2 2018. While promotions and offers during the festive Ramadan month contributed to the growth, the strong double digit growth is also due to the the fact,that during Q2 last year, the market was adapting to the local manufacturing terms and conditions (TKDN)

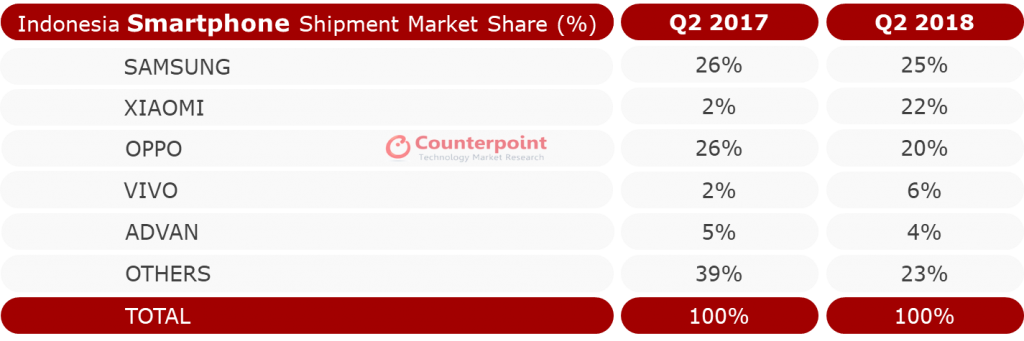

- Samsung led the smartphone segment with a market share of 25% followed closely by Xiaomi and OPPO.

- Xiaomi became the second largest brand in Indonesia. Xiaomi now has a broader portfolio as compared to a year ago. Moreover, it has managed to reduce the gap of popular global products and their launch in Indonesia which helped it to lead the sub $150 segment.

- OPPO had strong offline promotions around its F series which drove volumes. Additionally, its A83 and A71 did well.

- The market share of Chinese brands reached 53% (the highest ever) in Indonesia with local brands at 9%.

- LTE capable smartphones contributed to 90% of total smartphone shipments during Q2 2018. Indonesian operators have done well in increasing the LTE coverage ahead of the 2018 Asian Games.

- Mid end segment has the largest number devices being launched with brands attracting users through offers like trade-ins, data bundling and higher memory capacity options for similar SKUs.

- Sub $150 segment contributed to over half of the market. $100-$150 segment was the fastest growing price band.

- Apple had less than 1% market share in country. Apple has recently expanded its reach in the country, but new iPhones are still expensive in the region.

- Qualcomm led the SoC segment with 39% market share followed by MediaTek and Samsung with 30% and 20% share respectively.

- Other brands which did well during the quarter were vivo, Asus and Huawei.

Exhibit 1: Indonesia Smartphone Shipments Market Share in Q2 2018

Source: Counterpoint Research Market Monitor Q2 2018

The comprehensive and in-depth Q2 2018 Market Monitor is available for subscribing clients. Please feel free to contact us at press(at)counterpointresearch.com for further questions regarding our latest research or insights. The Market Monitor research is based on sell-in (shipments) estimates based on vendor’s IR results, vendor polling triangulated with sell-through (sales), supply chain checks and secondary research. Analyst Contacts: Tarun Pathak +91 997-121-3665 [email protected] Parv Sharma +91 974-259-6030 [email protected] Follow Counterpoint Research press(at)counterpointresearch.comReceive our insightful weekly newsletter and stay ahead of the competition.

Author

Tarun Pathak

Tarun is a Research Director with Counterpoint Research, based out of Gurgaon (near New Delhi). Tarun has 10 years of work experience with a key focus on the evolving mobile device ecosystem with specialties in Emerging Markets. He understands specific mobile industry nuances, helping clients to navigate through the rapidly changing technological trends. As a Telecom Analyst he has been quoted extensively by the leading media platforms. Tarun holds a Post Graduate Diploma in Management, specializing in International Business from the Amity International Business School and is a graduate in Physical Sciences from Jammu University, Jammu in the northern Indian state of Jammu & Kashmir.