Insight

Xiaomi IPO : Need Focus on Intellectual Property & Opportunities

0

May 3, 2018

- It is a historical day for the eight year old upstart Chinese consumer electronics vendor Xiaomi as it filed for its Initial Public Offering (IPO) in Hong Kong

- The company aims to raise several billion dollars which could drum up its valuation to tens of billions of dollars (see here - Further Analysis by Richard Windsor)

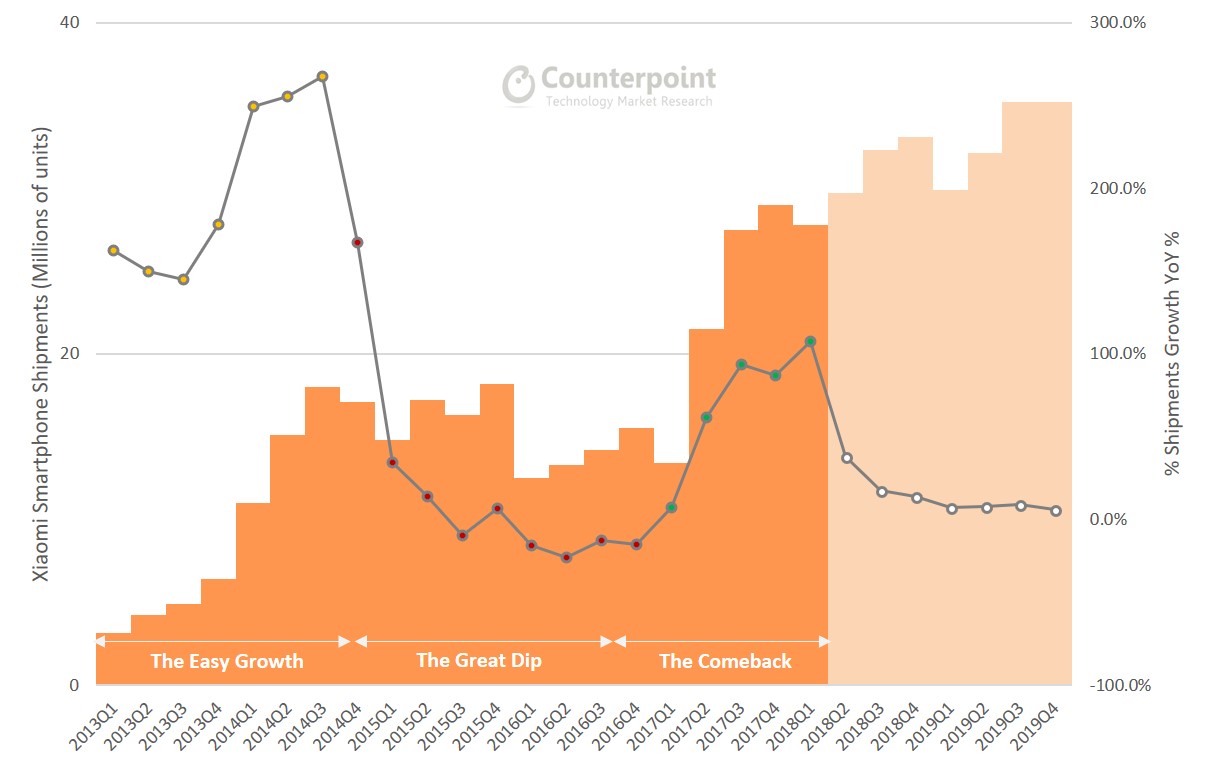

- The timing is perfect for Xiaomi, as it made a strong comeback into its core segment of selling smartphones in 2017 after falling off the cliff in 2016, which is very rare in the mobile phone industry.

- Xiaomi was the fastest growing brand in CY2017 with smartphone shipments surging 56% YoY (see here)

Source: Xiaomi

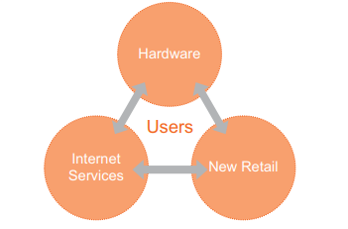

- Xiaomi reiterates being a "low-cost"player with the founder Lei Jun vowing to keep the hardware margins below 5%

- Xiaomi essentially subsidizes or maintains a relatively low margin on hardware to bring more users into its ecosystem

- Players such as Google or Facebook give away free services or software to acquire users (but TACs are much lower and margins quite high)

- Xiaomi's acquisition strategy is relatively costlier, but somewhat works in a commoditized or price-sensitive market

- Xiaomi over eight years had amassed more than 170 million MAUs in its ecosystem by the end of 2017

- According to Xiaomi, a Xiaomi user spends atleast 4.5 hrs a day on their Xiaomi device, which opens up an opportunity for Xiaomi to monetize

- Once Xiaomi acquires its users, it tries to attract them to use or subscribe to their digital services from content to cloud, leveraging its MIUI OS built on top of Android (AOSP)

- This works quite well in China where the bulk of the usage comes via its own version of OS, due to absence of the Google Play store.

- With this strategy, Xiaomi generated more than US$1.5 Billion in revenues in 2017 from its services segment

- The Services segment, however, contributed to just 9% of the total revenues which is still minuscule, to tout the premise of services-driven business model

- Having said that, Xiaomi is seeing around 60% gross margins on services, compared to a mere 9% gross margins on hardware, so it is definitely a lucrative segment, if they can scale it significantly

- The current ARPU for services business was close to US$9 per year in 2017, which is slightly low when compared to other internet or integrated players

- However, Xiaomi also looks to other opportunities beyond smartphones by cross-selling its IoT & Lifestyle products via its retail strategy e.g. Air Purifiers, Smart TVs, Weighing scales, Smart Home solutions, etc.

- The rough average spending on IoT Lifestyle devices is close to US$40 per year per smartphone shipped in 2017, though at relatively lower gross margins than services

- This is how the business model for Xiaomi works, but at relatively lower margins and potentially could be replicated by other deep pocketed, bigger scale players such as Huawei or Samsung or BBK

- This is a chink in Xiaomi's armor from a business model robustness perspective, as it is hardly based on any sort of IP or differentiating R&D which would not amuse many investors to begin with

Xiaomi's pre-IPO performance

- Xiaomi started off well in its early phase with an ascent for the first three years, post which competitors such as Huawei and others caught up in terms of low-cost + ecommerce business model and slowed down Xiaomi's growth

- Further, lack of IP and scale also hurt the supply chain to procure key components to meet demand if any for some hit models in 2015 and 2016.

- However, this was streamlined by early 2017 which was one of the reasons for the growth spurt

- India the second largest smartphone market (see here) has been the key reason for Xiaomi to make a comeback, as competition fizzled out in online space and the "value for money" products from Xiaomi hit the right note with price-sensitive growing middle class Indian consumers

- Online segment was important in India because almost a third of country's smartphones are sold online and Xiaomi raced to capture close to half of that segment (see here)

- Further, during the year Xiaomi also expanded its reach beyond India and China and started shipping to 72 other markets globally in 2017. This also drove some uptick in volumes and decreased dependency on the Chinese market where it has been struggling against Huawei's Honor, OPPO and vivo brands

- However, smartphones still contribute to almost 70% of the total Xiaomi revenues, which climbed to US$18 Billion in 2017 up 68% annually

- Smartphones (+65% YoY) and IoT/Lifestyle (+88% YoY) grew faster than the important Services segment (+51% YoY) in 2017

- Having said that, the hardware growth drove the overall installed base of Xiaomi devices higher, which it will look to monetize during the devices' lifetime

- Xiaomi has the momentum in hardware in India, so will continue with “India first” strategy and build hardware as well as services (e.g. content) ecosystem in India and scale it elsewhere

- Obviously, Xiaomi has also entered other developing markets in Europe and Asia last year. Further expansion plans in Africa and Latin America later this year, will drive the global installed base for the Chinese vendor

Why IPO?

- Scaling its razor-thin margin business model of acquiring users using low-cost hardware, requires consistent capital infusion.

- Further, to differentiate, Xiaomi has to build an Intellectual Property (IP) arsenal, and thus has to consistently invest in R&D. This requires significant capital, but is not possible with thinner gross margins

- Whereas players such as Apple, Google, Amazon or Facebook have significantly higher gross margins and are able to consistently re-invest into R&D to differentiate and scale

- Xiaomi will also need capital to invest in developing AI technologies and related infrastructure to process all the data coming from close to a couple of hundred million users to help it build meaningful services and differentiated experiences

- With this IPO, we can see Xiaomi using this capital to scale to more markets globally, which demands greater localized investments and expenses

- At the same time, Xiaomi will have to be prudent about not spending too much capital on subsidizing devices further or on marketing or channel development initially

- This is not possible with sporadic private rounds of funding, hence, Xiaomi needs to go public for a more crowd-sourced capital infusion

- This also gives Xiaomi an opportunity to acquire key companies and become more integrated like Huawei or Samsung or Apple

- Additionally, we believe since Xiaomi is riding high on a wave which prompts exiting investors also to push for Xiaomi to go public and the initial investors thus can cash in on the potential leap in valuation

- In a nutshell, Xiaomi should look to focus on opportunities to grow its service business which is very central to its business model, expand into newer markets and above all focus more on R&D and IP development

Receive our insightful weekly newsletter and stay ahead of the competition.

Author

Neil Shah

Neil is a sought-after frequently-quoted Industry Analyst with a wide spectrum of rich multifunctional experience. He is a knowledgeable, adept, and accomplished strategist. In the last 18 years he has offered expert strategic advice that has been highly regarded across different industries especially in telecom. Prior to Counterpoint, Neil worked at Strategy Analytics as a Senior Analyst (Telecom). Neil also had an opportunity to work with Philips Electronics in multiple roles. He is also an IEEE Certified Wireless Professional with a Master of Science (Telecommunications & Business) from the University of Maryland, College Park, USA.