Global Smartphone Market Grows 8% YoY In Q2 2024; ASP Reaches Highest Level For a Second Quarter

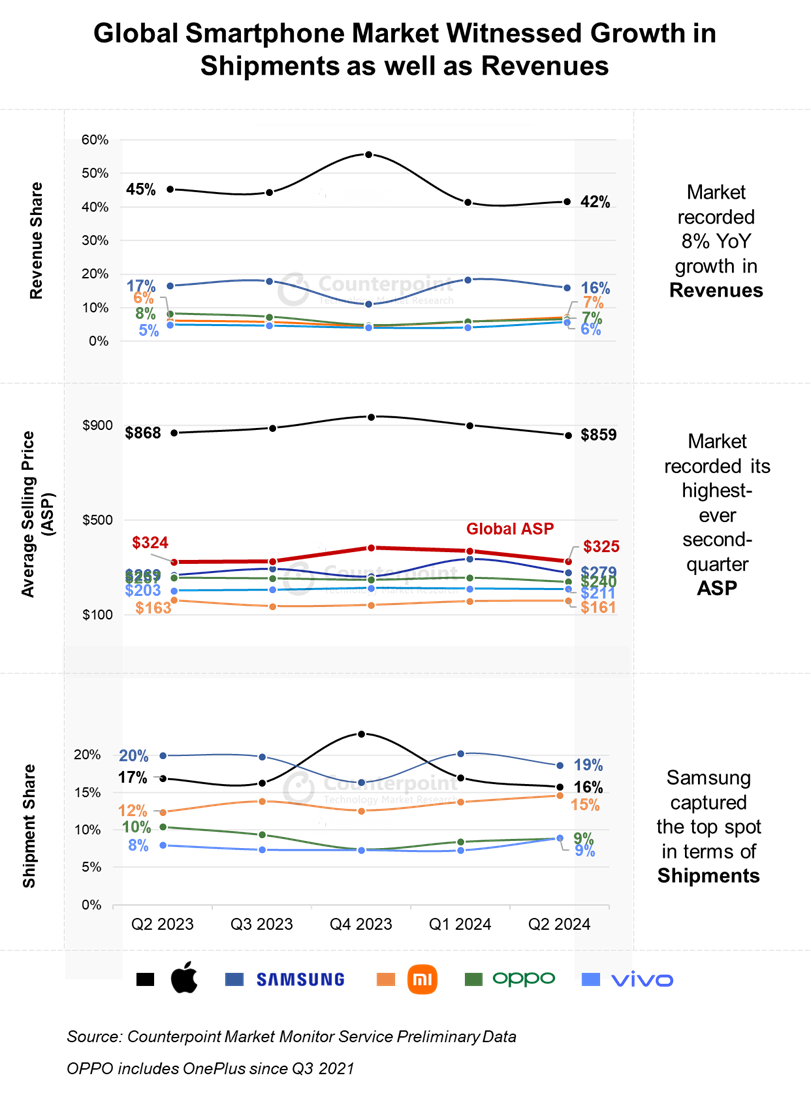

- The global smartphone market grew by 8% YoY to reach 289.1 million unit shipments in Q2 2024.

- Samsung retained the top position globally, accounting for 19% shipment share.

- Apple’s shipments registered marginal growth in Q2 2024, however, it led the revenues with 42% share.

- Among the top five OEMs, Xiaomi grew the fastest, registering 27% YoY shipment growth.

- Global smartphone revenues also grew 8% YoY, while the ASP reached the highest level for a second quarter.

Seoul, Beijing, Boston, Buenos Aires, Fort Collins, Hong Kong, London, New Delhi, Taipei, Tokyo – August 2, 2024

Global smartphone shipments grew 8% YoY in the second quarter of 2024, according to the latest research from Counterpoint’s Market Monitor service. Almost all the regions registered growth, owing to improving consumer sentiment and macroeconomic conditions. This marks the third consecutive quarter posting growth for the global smartphone market. Commenting on overall market dynamics, Senior Analyst Prachir Singh said, “Smartphone shipments registered strong growth as key regions continued on a recovery path. Caribbean and Latin America (CALA) emerged as the fastest growing region as Chinese OEMs continued their aggressive push helped by increased demand in smaller markets in the region. Europe and Asia Pacific also registered double-digit growth. The China market grew thanks to a strong performance in the 618 sales, which included significant price discounts including Apple iPhone. And consumer sentiment improved in many European markets, reflected in the growth of smartphone shipments in the region, especially in Western Europe (WE), which grew faster than Central and Eastern Europe (CEE). Middle East and Africa (MEA) also registered single-digit growth due to a more favourable economic environment as well as increasing push from Chinese OEMs. However, India witnessed a marginal decline due to a seasonal slump aggravated by a severe heatwave.” Global smartphone revenues also grew by 8% YoY in Q2 2024. Apple led the smartphone market revenues with a 42% share. Samsung’s revenues grew 5% YoY, due to growth in its ASP as well as shipments. Among the top five OEMs, Xiaomi’s revenue growth was the fastest in a second consecutive quarter as it maintained a strong performance in its key markets. Revenues for the market beyond the top five OEMs also grew significantly, driven by increasing revenues from Huawei, HONOR, Motorola and Transsion brands. The >$800 segment continued to increase its share, growing YoY by 2pp, while taking share from sub-$400 segments.

Global smartphone revenues also grew by 8% YoY in Q2 2024. Apple led the smartphone market revenues with a 42% share. Samsung’s revenues grew 5% YoY, due to growth in its ASP as well as shipments. Among the top five OEMs, Xiaomi’s revenue growth was the fastest in a second consecutive quarter as it maintained a strong performance in its key markets. Revenues for the market beyond the top five OEMs also grew significantly, driven by increasing revenues from Huawei, HONOR, Motorola and Transsion brands. The >$800 segment continued to increase its share, growing YoY by 2pp, while taking share from sub-$400 segments.

Commenting on Apple’s performance, Research Director Jeff Fieldhack said, “There were worries that iPhone volumes would disappoint after North American carriers reported record low upgrade rates and lower iPhone sales. We estimate Apple iPhone volumes were flat and revenue declined by 1% YoY despite Pro series sales growth. Apple’s China sales was down 6.5%, but it could have been a lot worse. Apple's China sales improved due to attractive discounts offered during the 618 shopping festival. The outlook for Apple looks solid as there is more supply chain excitement for the upcoming iPhone 16 family and big expectations for Apple Intelligence.”

Samsung led global smartphone shipments during the quarter, driven by the strong performance of Galaxy A-series as well as continued momentum of Galaxy S24 series. According to our latest report, Samsung captured five spots in the top 10 best-selling smartphones. Among the top five brands, Xiaomi was the fastest growing brand followed by vivo. For Xiaomi, MEA and CALA regions were the major growth drivers, while it also gained momentum in its traditional markets like China, India and key APAC countries. While, for vivo, China remained the major growth driver along with India and South-Asian countries. Huawei, HONOR, Motorola and Transsion were the other key brands that gained during the quarter. Huawei continued its strong momentum in China which was the major reason for its growth. HONOR gained in CALA and MEA, in addition to having a strong share in China. The Transsion brands, TECNO, itel and Infinix, performed strongly in Eastern Europe, India and MEA. India, CALA and North American markets were the growth drivers for Motorola. OPPO* experienced a marginal shipment decline, mostly due to a decline in OnePlus’s shipments. OnePlus is experiencing stiff competition in its key markets.

Commenting on the near-term outlook, Research Director Tarun Pathak said, “In terms of shipments, we see a gradual recovery for the global smartphone market. The ongoing premiumization trend, coupled with the AI trend, is likely going to push up the ASPs and revenues in the coming quarters. Smartphones make the perfect platform for making AI accessible to everyone. Generative AI, especially, is revolutionizing smartphones. It offers personalized experiences, enhances existing features, and allows for more intuitive interactions. We estimate that GenAI’s share of overall smartphone shipments will reach 18% by 2024.”

*OPPO includes OnePlus since Q3 2021

Note: Pricing analysis is based on wholesale prices.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

Follow Counterpoint Research

press(at)counterpointresearch.com

Commenting on Apple’s performance, Research Director Jeff Fieldhack said, “There were worries that iPhone volumes would disappoint after North American carriers reported record low upgrade rates and lower iPhone sales. We estimate Apple iPhone volumes were flat and revenue declined by 1% YoY despite Pro series sales growth. Apple’s China sales was down 6.5%, but it could have been a lot worse. Apple's China sales improved due to attractive discounts offered during the 618 shopping festival. The outlook for Apple looks solid as there is more supply chain excitement for the upcoming iPhone 16 family and big expectations for Apple Intelligence.”

Samsung led global smartphone shipments during the quarter, driven by the strong performance of Galaxy A-series as well as continued momentum of Galaxy S24 series. According to our latest report, Samsung captured five spots in the top 10 best-selling smartphones. Among the top five brands, Xiaomi was the fastest growing brand followed by vivo. For Xiaomi, MEA and CALA regions were the major growth drivers, while it also gained momentum in its traditional markets like China, India and key APAC countries. While, for vivo, China remained the major growth driver along with India and South-Asian countries. Huawei, HONOR, Motorola and Transsion were the other key brands that gained during the quarter. Huawei continued its strong momentum in China which was the major reason for its growth. HONOR gained in CALA and MEA, in addition to having a strong share in China. The Transsion brands, TECNO, itel and Infinix, performed strongly in Eastern Europe, India and MEA. India, CALA and North American markets were the growth drivers for Motorola. OPPO* experienced a marginal shipment decline, mostly due to a decline in OnePlus’s shipments. OnePlus is experiencing stiff competition in its key markets.

Commenting on the near-term outlook, Research Director Tarun Pathak said, “In terms of shipments, we see a gradual recovery for the global smartphone market. The ongoing premiumization trend, coupled with the AI trend, is likely going to push up the ASPs and revenues in the coming quarters. Smartphones make the perfect platform for making AI accessible to everyone. Generative AI, especially, is revolutionizing smartphones. It offers personalized experiences, enhances existing features, and allows for more intuitive interactions. We estimate that GenAI’s share of overall smartphone shipments will reach 18% by 2024.”

*OPPO includes OnePlus since Q3 2021

Note: Pricing analysis is based on wholesale prices.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

Follow Counterpoint Research

press(at)counterpointresearch.com

Receive our insightful weekly newsletter and stay ahead of the competition.

Author

Team Counterpoint

Counterpoint Research is a global industry and market research firm providing market data, intelligence, thought leadership and consulting across the technology ecosystem. We advise a diverse range of global clients spanning the supply chain – from chipmakers, component suppliers, manufacturers and software and application developers to service providers, channel players and investors. Our veteran team of analysts serve these clients through our offices located across the key innovation hubs, manufacturing clusters and commercial centers globally. Our analysts consistently engage with C-suite through to strategy, market intelligence, supply chain, R&D, product management, marketing, sales and others across the organization. Counterpoint’s key coverage areas: AI, Automotive, Cloud, Connectivity, Consumer Electronics, Displays, eSIM, IoT, Location Platforms, Macroeconomics, Manufacturing, Networks & Infra, Semiconductors, Smartphones and Wearables.