Insight

Cloud Server CAPEX Soars as Datacenter Companies Look to Increase Share in Cloud Services Market

0

August 8, 2019

The cloud services market has been experiencing high double-digit growth in the past few years. Yet, there is more room to grow. Demand will continue to increase as more geographies, and companies adopt cloud services. Conventional corporate organizations are shifting towards public and hybrid cloud due to better offerings and low-cost maintenance. This demand has compelled datacenter and IaaS (Infrastructure-as-a-Service) providers to invest heavily and continually increase their infrastructure to support clients.

Among the Cloud Services providers who spend for servers and related hardware, Google dominated followed closely by AWS in 2018 (Exhibit 1). According to Counterpoint’s Cloud Services Tracker, Google spent 10% of the overall global spend, followed by Amazon Web Services (AWS) and Alibaba, with 9% and 7% share, respectively, in 2018. Facebook and Microsoft are also spending heavily to increase their datacenter capacities and capabilities. Other notable players are Apple, Intel, IBM, China Telecom, and Equinix.

Exhibit 1: Cloud Infrastructure CapEx Spend – 2018

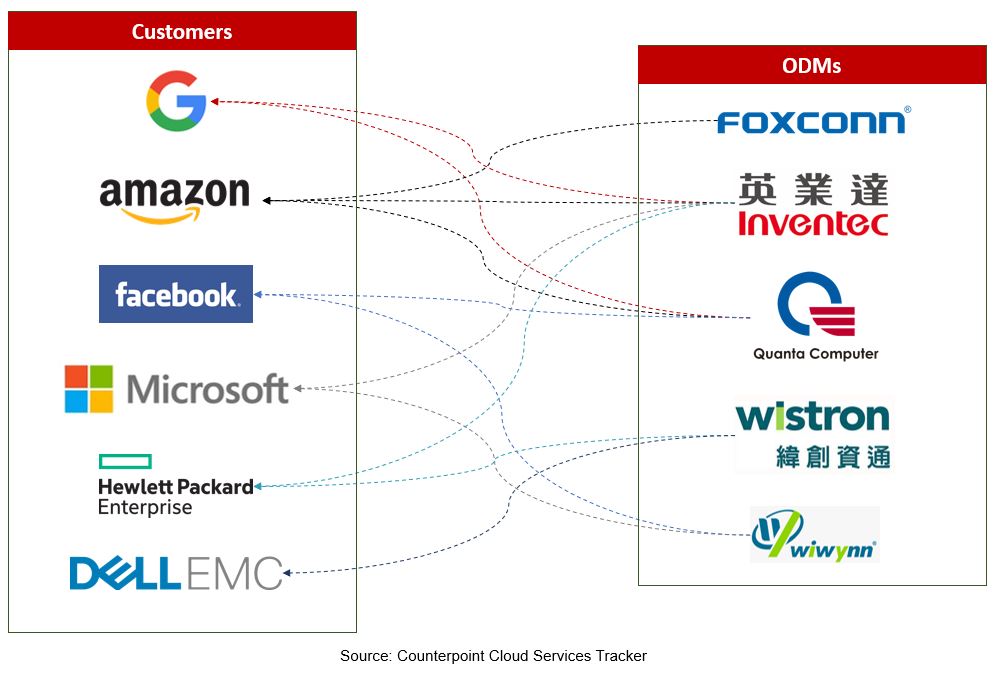

Further, Counterpoint’s Cloud Services Tracker shows that the combined capital expenditure (CAPEX) of FAMGA (Facebook, Apple, Microsoft, Google, Amazon) increased by 45% year-on-year (YoY) in 2018. Intel’s CAPEX rose by 29% YoY in 2018. Chinese counterparts, BAT (Baidu, Alibaba, Tencent) and China Telecom saw a 24% YoY increase in CAPEX. Combined, FAMGA, Intel, BAT, and China Telecom contributed to 56% of global CAPEX by datacenter and IaaS providers. Among the REITs (Real Estate Investment Trusts), Equinix and Digital Realty are the biggest contributors. However, going forward, we expect the CAPEX of cloud services providers to increase as companies like Google and Microsoft venture into cloud gaming by launching their platforms, Stadia and Project xCloud, respectively. AWS has the most number (66) of cloud infrastructure locations worldwide with 12 more locations in the pipeline, followed by Google Cloud with 61 such locations. Alibaba has 58 locations worldwide while Microsoft Azure has 20. These cloud giants are expanding globally as they look to increase their market share in the cloud services market. Further, these companies are working to ramp up their product portfolio with innovations and acquisitions and increase their market share by engaging in strategic partnerships. Google has been quite aggressive in expanding its cloud services through acquisitions. Recently, it has acquired Looker, a big data and analytics platform, for a massive US$2.6 billion. Google’s list of acquisitions includes Qwiklabs, Kaggle, Bitium, Apigee, and Orbitera, among others. AWS is also active in this regard and has acquired companies like 2lemetry, Elemental, ClusterK, Cloud9 IDE, Graphiq and Sqrrl, among others. AWS even acquired Annapurna Labs to boost its internal production of custom chips for cloud infrastructure. Further, cloud services providers are partnering with Taiwanese/Chinese ODMs to source servers and other components for increasing their capacities. The biggest ODM contributors are Foxconn, Wistron, Wiwynn, Inventec, Quanta providing servers to Google, Facebook, Microsoft, Amazon, and OEMs such as Hewlett Packard Enterprise (HPE) and Dell. Inventec and Quanta have the highest number of partnerships with leading cloud providers. Exhibit 2 shows the customer-ODM relationships.

Exhibit 2: Cloud Provider/OEM – ODM Partnerships

The future looks bright for the ODMs, server OEMs, as well as component makers as cloud providers, continue to expand their consumer base as well as services. Multiple new services such as cloud gaming, service mesh, IoT expansion as well as entry into new geographies will drive the cloud adoption and hence, will increase the infrastructure spend by cloud service providers.

Receive our insightful weekly newsletter and stay ahead of the competition.

Author

Prachir Singh

Prachir is a Senior Research Analyst at Counterpoint Research based out of Gurgaon. In Counterpoint, he closely tracks mobile devices and ecosystem. He also tracks Emerging Tech Opportunities. He has a total of 10+ years of experience across various sectors like manufacturing, management consulting, strategy and operations. He is an engineering graduate from Indian Institute of Technology (IIT), Kharagpur.