ASML’s 2024 Revenue Hits Record High, Logic Segment to Lead in 2025

- System sales increased 25% as momentum picked up in H2 2024, while Installed base and services grew by 38% YoY during the quarter.

- Revenue contribution from China increased 40% YoY; US and Japan’s contributions increased in H2 2024.

- Logic segments will drive further growth in 2025, memory segment to be flat.

- Order intake to remain elevated in H1 2025 as 2nm production ramps up.

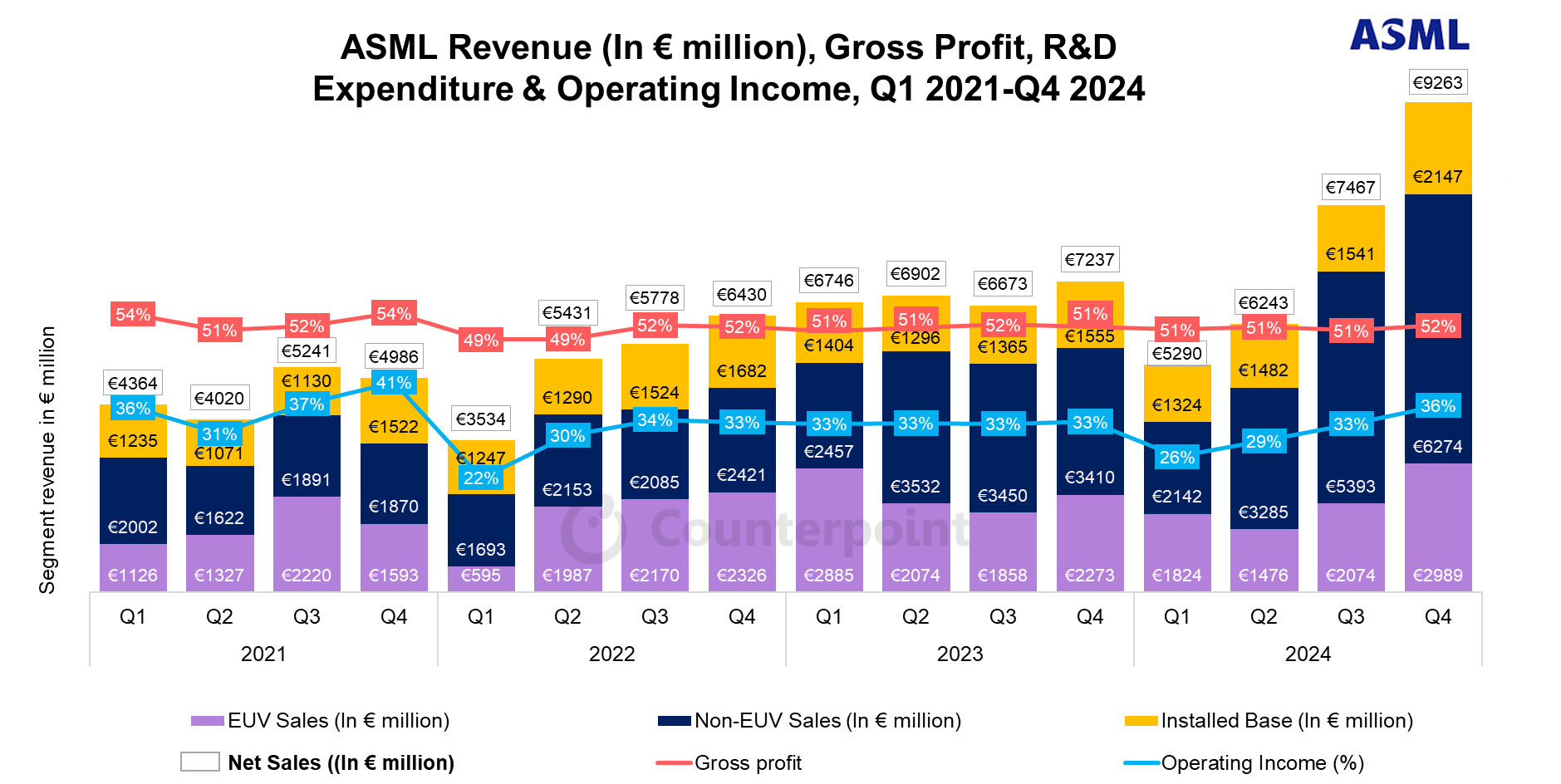

ASML’s 2024 revenue climbed about 3% YoY to hit an all-time high of €28.3 billion, driven by record high sales during the final quarter of the year. The company’s Q4 2024 net sales increased to €9.3 billion, driven by a 16% YoY increase in installed base revenue. Its Memory segment accounted for 39% of the system sales, rising 43% YoY to €2.8 billion during the quarter, while the Logic segment rose to €4.3 billion. Revenue contribution from China reached a record 41% in 2024, although it is expected to normalize to low 20% in 2025.

Commenting on AI enhancements, ASML CEO Christophe Fouquet said, “The semiconductor market remains strong with AI spurring growth but also a shift in market dynamics. These dynamics will lead to a shift in the mix of end-market products towards more HPC and HBM which requires more advanced Logic and DRAM.”

Analysis:

ASML’s order bookings rose to €7.1 billion in Q4, with €3 billion coming from the EUV segment, which is key to making high-performance chips. With tool lead times of 12 to 18 months, orders will likely stay strong in early 2025. Demand will further increase as 2nm production starts in late 2026 and scales in 2027, driven by AI adoption in smartphones, HPC, PCs, and servers. The rise of AI models like DeepSeek is fueling competition and the need for more advanced chips is inevitable, pushing semiconductor firms to upgrade technology across logic, DRAM, and NAND to keep driving revenue growth for tool makers.

Commenting on the export regulations, ASML CFO Roger Dassen said, “The combination and the impact of both US and Dutch measures has been appropriately reflected in the guidance that we have given before. So, the €30 billion to €35 billion properly reflects the limitations that we see from current export controls perspective.”

Analysis:

The latest round of US sanctions broaden the scope of restrictions to include additional semiconductor manufacturing equipment such as etch, deposition, lithography, ion implantation, and metrology tools. High-bandwidth memory (HBM), critical for advanced AI applications, also falls under these new restrictions.

The new restrictions are expected to slow China’s progress in developing advanced AI systems, as HBM is crucial for both training and inference at scale. Additionally, the inclusion of tools like deposition, etch, and metrology in the regulations will impede the manufacturing of advanced nodes, challenging Chinese firms like SMIC, which have been creatively leveraging DUV equipment to achieve leading-edge nodes.

Result Summary

Revenue Highlights

ASML’s Q4 2024 revenue rose 28% YoY to reach a record high of €9.3 billion. The increase was mainly due to the increase in system sales, as the demand for memory and logic chips is increasing, and also due to an increase in service and installed base revenue.

R&D investments increased 7% YoY to €1.1 billion during the quarter, accounting for 12% of total revenue. The gross margin was 52% during the period, increasing by 29% YoY due to an increase in sales contribution from EUV.

Taiwan, China, and South Korea accounted for around 62% of ASML’s total revenue during the quarter. US and Japan’s revenue contribution increased significantly on account of multiple fabs that opened in the region.

System sales increased by 25% YoY to 7.1 billion, and EUV accounted for 42% of the system revenue during the quarter. The Logic segment grew by 21% YoY while Memory grew 32% YoY as demand for HBM increased to cater to the highly computational AI data centers.

Net booking for the quarter reached €7.1 billion with the logic segment accounting for 61% of the gross bookings.

For 2024, net revenue increased by 3% YoY to €28.3 billion. China, USA, and Japan were some of the regions that reported double-digit YoY percentage growth.

EUV sales started to increase: EUV accounted for 38% of the net system sales in 2024, down from 42% in 2023, although it started increasing from Q4 2024 onwards with demand for High-NA EUV increasing among the customers both for advanced logic and memory chips.

Order book rose to €7.1 billion: The order book rose to €7.1 billion, driven by increasing orders from the logic segment which constituted 61% of the orders during the quarter, as the demand for advanced and mature nodes increased across regions. Memory segment accounted for 39% of the order book, as the demand for HBM has increased to support the LLM models.

Revenue contribution from shipments to China increased the most in 2024: Net system revenue from China increased by 40% YoY to €8.9 billion and accounted for 41% of ASML’s net system sales in 2024, up from 29% in 2023, driven by increased demand for mid-critical and mature nodes. During H2 2024, China accounted for 36% of ASML’s sales. For 2025, China revenue will normalize to low 20% partially due to export control and mostly due to exhaustion of previous backlog on account of strong China sales in the previous two years.

USA, Japan, and South Korea are the next growth regions: US net system sales increased 69% YoY to €3.7 billion and increased by 98% YoY for Japan to €0.87 billion for 2024, on account of TSMC opening new Fabs across regions, as they are diversifying their supply chain. Although South Korea’s contribution to revenue decreased to 21% in 2024 to €4.6 billion, it started increasing from Q4 2024 onwards due to adoption of EUV by memory chipmakers.

2024 is a record year: ASML reported record revenue in Q4 2024 and full year 2024, driven by increased system sales in the latter half of the year. AI’s growth is transitioning the industry, with increased demand for advanced nodes and HBM. Increased installed base revenue and a pickup in momentum in system sales in H2 2024 drove a 28% YoY increase in net revenue. US and Japan’s 2024 system sales increased 1.5x and 3x, respectively, as compared to 2023 with momentum picking up in H2 2024 due to multiple fabs opening in the region.

Strong acceleration expected in 2025: 2025 net revenue is expected to be in the range of €30 billion to €35 billion with gross margin between 51% and 53%. AI will likely to be a major driver in 2025, and it will increase demand in the Logic segment more than in Memory. With lead times more than 12 to 18 months, order intake will remain elevated in H1 2025 as 2nm production ramps up going into H2 2026. China revenue will normalize to low 20% partially due to export control and mostly due to exhaustion of the previous backlog on account of strong China sales in the previous two years. Growing systems installed base will provide high value service and upgrades will drive double-digit percentage growth in 2025 installed base revenue. Revenue recognition of high-NA systems in H2 2025 will drive a decline in gross margins.

Receive our insightful weekly newsletter and stay ahead of the competition.

Author

Team Counterpoint

Counterpoint Research is a global industry and market research firm providing market data, intelligence, thought leadership and consulting across the technology ecosystem. We advise a diverse range of global clients spanning the supply chain – from chipmakers, component suppliers, manufacturers and software and application developers to service providers, channel players and investors. Our veteran team of analysts serve these clients through our offices located across the key innovation hubs, manufacturing clusters and commercial centers globally. Our analysts consistently engage with C-suite through to strategy, market intelligence, supply chain, R&D, product management, marketing, sales and others across the organization. Counterpoint’s key coverage areas: AI, Automotive, Cloud, Connectivity, Consumer Electronics, Displays, eSIM, IoT, Location Platforms, Macroeconomics, Manufacturing, Networks & Infra, Semiconductors, Smartphones and Wearables.